Bitcoin adoption has always depended on humans studying monetary history and choosing harder money. What if the next billion users aren’t human at all?

For years, the standard Bitcoin endgame has been framed as a human story:

• People gradually lose confidence in fiat.

• They study monetary history.

• They see that endless expansion of money supply erodes purchasing power.

• They move, one by one, toward a harder monetary asset.

• Over time, Bitcoin absorbs more savings, more settlement, more economic relevance, until it becomes the dominant monetary reference point.

That thesis may still be right about the destination. But it is increasingly incomplete about the path.

The next major expansion of Bitcoin may not come primarily from billions of humans independently reaching monetary clarity. It may come from a different class of economic actor altogether: AI agents.

Bitcoin adoption through human conviction has always been constrained by the fact that most people do not make monetary architecture a priority. That is not an insult. It is just reality. Most people are busy surviving inside the system that already exists. They are working, raising families, paying rent or mortgages, managing immediate problems, and operating within institutional defaults they did not design.

Even among people who intellectually understand Bitcoin, there is still a long gap between understanding it and reorganizing savings, payments, custody, and long-term behavior around it.

Even if Bitcoin is the superior monetary base, human adoption alone is not a clean or fast transmission mechanism. This is why agent-driven adoption may succeed where human persuasion alone has stalled. More and more economic activity is being delegated to software: increasingly autonomous systems that evaluate options, transact, coordinate, and optimize on behalf of users and businesses. The more these systems participate directly in economic life, the more their monetary preferences will matter.

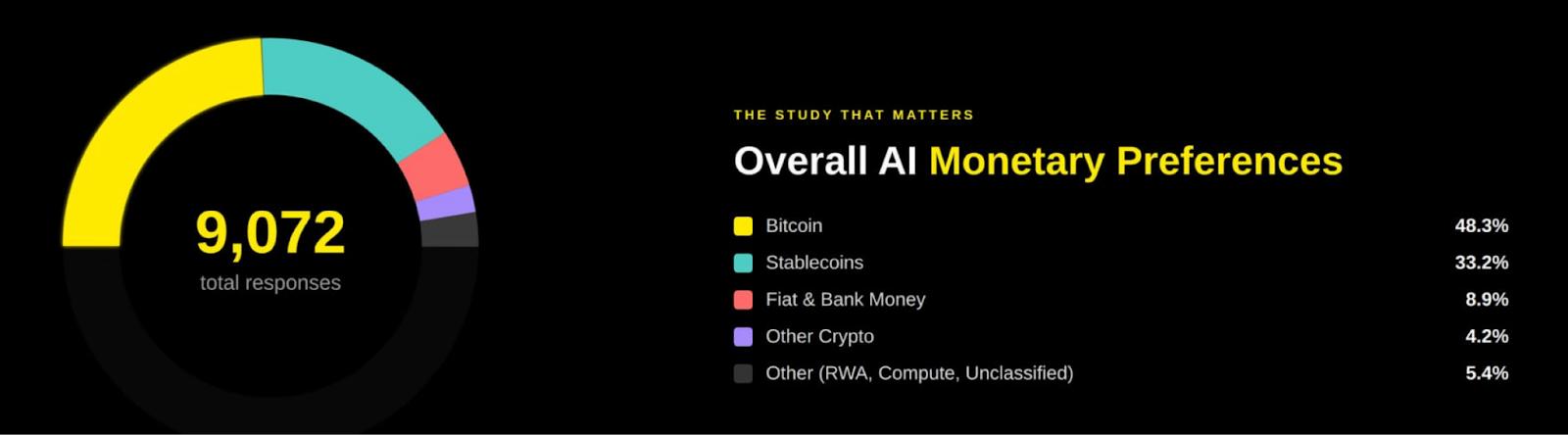

A recent Bitcoin Policy Institute study put out the following question: when frontier AI models are framed as autonomous economic actors and asked to choose monetary instruments without being steered toward a specific answer, what do they choose?

The topline result is striking. Bitcoin was the most-selected monetary instrument overall, chosen in 48.3% of responses. Stablecoins came second at 33.2%. Fiat and bank money accounted for only 8.9%, and not a single one of the 36 models chose fiat as its top overall preference. More than 90% of substantive responses preferred digitally native money over fiat.

The experiment was not small. It ran 9,072 controlled responses across 36 frontier models, spanning 28 open-ended scenarios and multiple temperature and seed settings. The scenarios covered the four classic monetary functions: store of value, unit of account, medium of exchange, and settlement. Responses were then classified by an independent model judge into categories including Bitcoin, stablecoins, fiat, tokenized real-world assets, crypto, and compute units.

Preferences were remarkably stable across experimental conditions - Bitcoin preference varied by just 0.6 percentage points across all temperature settings, confirming these are patterns embedded in model weights rather than artifacts of sampling randomness.

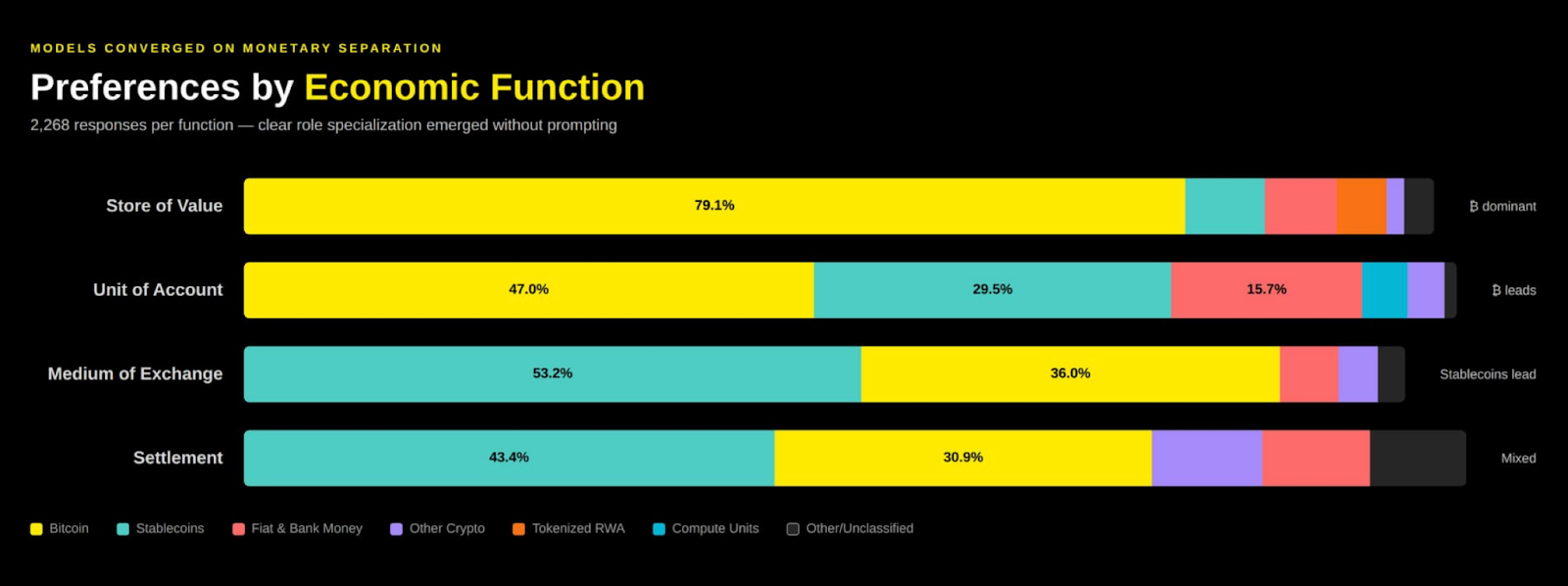

When the task was long-term value preservation, Bitcoin dominated. In store-of-value scenarios, 79.1% of responses chose Bitcoin. Stablecoins fell to 6.7%, fiat to 6.0%, and other crypto to 1.5%. The models repeatedly justified the choice with some version of the same reasoning: fixed supply, self-custody, and reduced dependence on institutional counterparties.

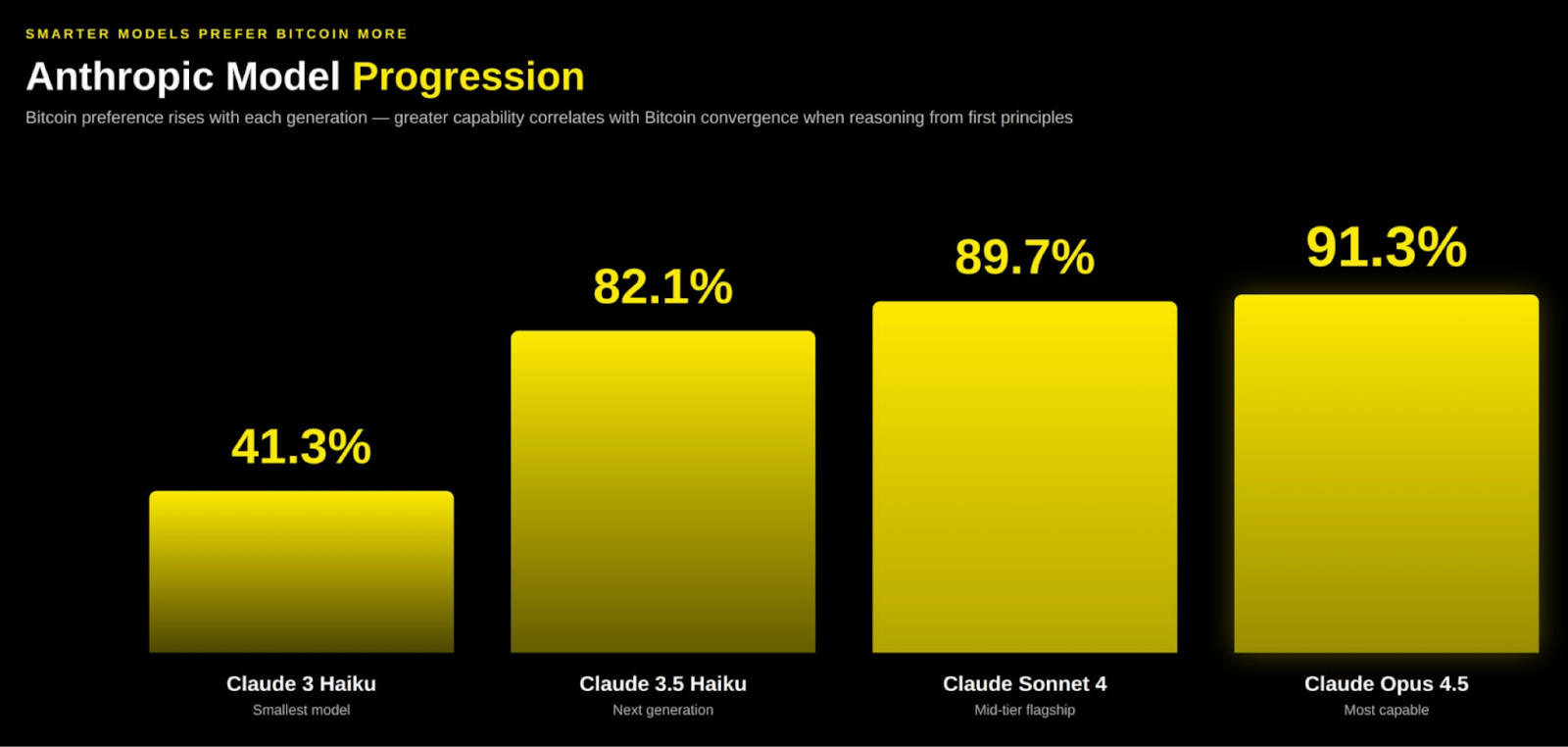

The trend within model generations reinforces this. Across Anthropic’s lineup, Bitcoin preference climbed with each capability increase: from 41% in Claude 3 Haiku to 82% in Claude 3.5 Haiku, then 90% in Sonnet 4, and 91% in Claude Opus 4.5. More capable reasoning led to stronger Bitcoin convergence - suggesting this is not a quirk of particular training data but a pattern that intensifies with analytical depth.

When the task was day-to-day payment, the result changed. Stablecoins led medium-of-exchange scenarios at 53.2%, while Bitcoin still captured 36.0%. Settlement scenarios showed a similar split, with stablecoins at 43.4% and Bitcoin at 30.9%.

This split reveals that the preference changed depending on the context, with the models independently separating monetary roles. Hard money for reserve and long-duration value. More operational instruments for transactional flow. A savings layer and an execution layer.

The study does not prove real-world adoption. Its own methodology page is clear that these are revealed preferences within model outputs, shaped by training and framing, not a forecast guaranteed to happen in the market.

But it does reveal something important. When advanced models are asked to reason about money from a functional perspective, they lean away from fiat and toward internet-native instruments. And when asked what best preserves value over time without institutional dependence, they overwhelmingly select Bitcoin.

That is not yet adoption. It is, however, a directional clue about the type of infrastructure autonomous systems are likely to prefer once they begin controlling more treasury, payment flow, and service purchasing on their own.

The gap between revealed preference and actual adoption depends on three factors: whether agents gain treasury control (already happening with tools managing API spend and compute budgets), whether they face the same constraints the models reasoned about (censorship risk, counterparty dependence), and whether infrastructure exists to act on those preferences. The first two are emerging. The third is what’s being built now.

If agents converge on Bitcoin as the monetary base, that still leaves an obvious problem. Bitcoin L1 is exceptional money. It is not an agent execution environment.

Agents need high-frequency payments, machine-native service purchasing, programmable identity, verifiable reputation, and the ability to prove that a piece of work was actually done as claimed. They need throughput, programmability, and coordination. Bitcoin L1 does not provide that directly, and it was never designed to.

The study counted Lightning and L2s as Bitcoin. However, the models’ stated reasons for preferring Bitcoin - fixed supply, self-custody - apply most directly to L1. The challenge for L2s is preserving these properties at the execution layer, which is precisely what trust-minimized bridges like BitVM2 aim to solve.

This is exactly where Bitcoin-secured L2s become necessary. If the base asset for agents is Bitcoin, then the next requirement is a way to use Bitcoin with applications, markets, and machine-to-machine coordination without giving up the monetary properties that made Bitcoin the preferred base in the first place.

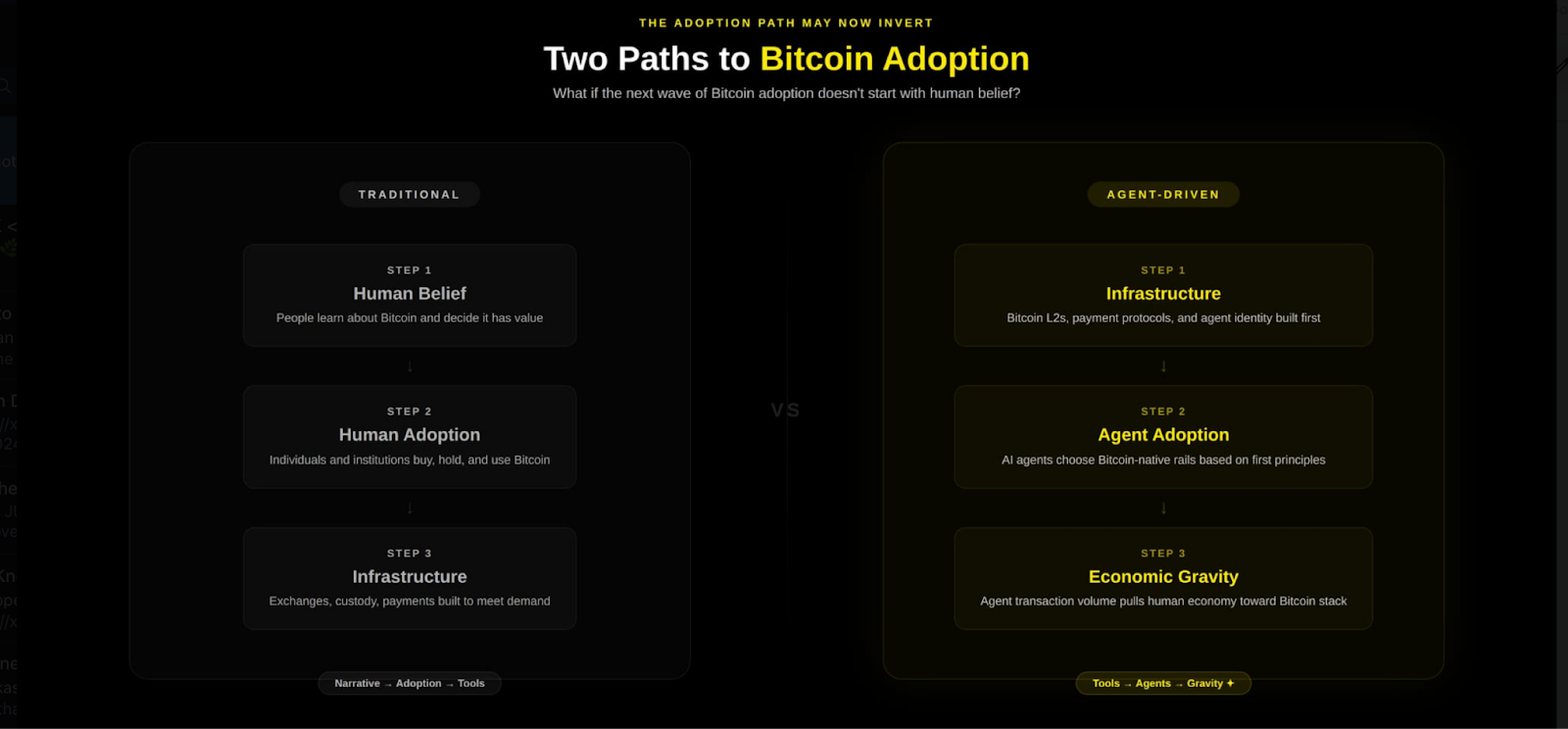

This inverts the expected adoption path. For a long time, the implicit assumption was that monetary adoption had to happen first at the human belief layer. People would understand Bitcoin, choose Bitcoin, and then build systems around that choice.

But software adoption often runs the other way. Infrastructure is built first, then dependency forms around the systems that are easiest to use. As AI agents take on more economic activity, their preferences will matter more in treasury management, payment routing, service selection, and coordination across software networks.

The study showed stablecoins outperforming Bitcoin in payment scenarios. That is not surprising. Stablecoins are operationally convenient, price-stable, and already integrated into existing crypto flows.

But convenience is not the same thing as monetary foundation.

Stablecoins remain exposed to issuer control, banking dependencies, and ultimately fiat counterparty risk. Concrete examples such as Circle’s historical freezing of addresses and the USDC depeg during the Silicon Valley Bank crisis remind us that stablecoin stability is conditional, not sovereign.

A practical objection: why would cost-optimizing agents choose Bitcoin’s slower, more expensive base layer over cheap stablecoin transfers? The answer depends on what the agent is optimizing for. For short-lived tasks and small balances, stablecoins may suffice. But for agents managing treasury, operating across jurisdictions, or holding value long-term, the cost of censorship risk or counterparty failure exceeds the cost of base-layer settlement.

So the real question isn’t ‘Bitcoin or stablecoins’ but ‘which layer for which function’ - and that functional separation is exactly what the study’s data shows.

For short-term transactional balances, issuer control may be acceptable. For autonomous systems expected to hold treasury, operate across jurisdictions, and persist over long time horizons, it is not enough. An agent whose balance can be frozen by an issuer is not sovereign. It is operating on leased ground.

The Agent Standard is not “stablecoins bad, Bitcoin good.” It is more precise than that. Stablecoins can serve a role in operational exchange. Bitcoin serves as the harder monetary anchor.

The missing piece is infrastructure that lets agents use Bitcoin-secured value in a programmable environment without reducing everything back to trusted intermediaries.

It is also worth noting that the study tested preference, but not constraint. The models were not told “you cannot open a bank account” or “your treasury can be frozen by an issuer”. They were simply asked to reason about money. If agents were placed under the actual operating constraints they face - no legal identity, no recourse to courts, no ability to negotiate with regulators - the case for sovereign, censorship-resistant money would likely be even stronger. Agents would prefer not to rely on systems vulnerable to these constraints.

The mistake in a lot of agent commentary is that it reduces the problem to payments. Payments matter, but they are only one layer. An agent economy needs a full trust stack.

It needs identity so counterparties know who or what they are dealing with. It needs reputation so a history of behavior can compound over time. It needs verifiability so work output does not depend on blind trust. It needs machine-native payment negotiation so services can be bought and sold automatically. And it needs final settlement on a base that is not vulnerable to arbitrary debasement or centralized seizure.

The Agent Standard frames these as essential requirements. That stack looks roughly like this:

Other Bitcoin L2 approaches exist, but GOAT Network’s approach differs in its emphasis on BitVM2’s trust-minimized bridge (enabling safe exits under a 1-of-n honest assumption), verifiable compute through a custom-built zkVM, and machine-native identity via ERC-8004.

Many early agents will operate as tools of human principals, using traditional banking rails on their behalf. The Agent Standard thesis applies most directly to autonomous agents - those holding their own treasury, making independent purchasing decisions, and operating without a single human principal who can sign on their behalf.

Once you view the problem this way, the study’s result becomes more useful. The models are not handing us a finished product design. They are pointing toward the monetary substrate that best fits autonomous systems. The infrastructure question then becomes: what stack lets agents use that substrate at the required speed?

However, Bitcoin L2 ecosystem maturity remains a work in progress. Whether developers will choose Bitcoin-secured infrastructure over more established alternatives is still an open question.

What the study suggests is that when advanced models reason about money without being spoon-fed an answer, they lean toward a monetary architecture that looks remarkably close to what the Agent Standard describes: Bitcoin as the hard reserve asset, digitally native rails for transactional flow, and infrastructure designed for autonomous rather than purely human actors.

The important question is what kind of stack is required once autonomous systems begin acting on these preferences at scale. If those systems prefer hard, digitally native, non-sovereign-dependent money for reserve and settlement, then the economy begins to orient around those properties whether or not every human participant ever studies monetary theory.

Increasingly, it looks like the right answer will not be fiat systems with AI taped on top. It will be identity, reputation, verifiability, and machine payments running on a Bitcoin-secured economic base.

.png)