In 2018, Saifedean Ammous published “The Bitcoin Standard”, a treatise on the economics of sound money. The core of his thesis was that fiat currency, unbacked and infinitely expandable, represents a degradation of money's essential properties. Bitcoin, he argued, restores monetary soundness through mathematical scarcity and cryptographic verification. The book became a foundational text for understanding why money must be independent of political control.

This work extends that argument into a new domain: autonomous agents. Just as humans require money free from government manipulation, machines require money free from human intermediation. The financial infrastructure we've built - banks, payment processors, regulatory frameworks - was designed for human participants with legal identities, liability structures, and recourse mechanisms. Autonomous agents operate under fundamentally different constraints.

An agent cannot open a bank account. It cannot sign a contract in a court of law. It cannot call customer service when a payment fails. It requires finality, not reversibility; determinism, not interpretation; availability, not business hours. Traditional finance treats these as bugs to be fixed. For agents, they are essential features.

This work defines what we call the Agent Standard: a set of monetary properties that autonomous machines require to participate as sovereign economic actors. We examine why traditional finance fails agents, why most cryptocurrency implementations fall short, and what properties agent-native money must possess. We trace the emergence of an agent economy and examine existing implementations of this standard. Finally, we address objections and clarify the thesis: this is not about a single network or protocol. It is about recognizing that machines need a different monetary architecture than humans, and that architecture must be built on the hardest money ever created.

The Bitcoin Standard gave humans sound money. The Agent Standard gives machines sovereign money.

The relationship between machines and money has evolved across three distinct eras, each expanding machine autonomy while maintaining human financial infrastructure. Understanding this progression reveals why current systems are inadequate for truly autonomous agents.

The first wave of machine-to-machine communication came through Application Programming Interfaces. Services like Twilio, SendGrid, and AWS allowed one machine to request services from another. A web server could programmatically send an email, process an image, or store data - all without human intervention in the transaction itself.

Yet every API call ultimately traced back to a human account holder. A machine could “initiate” a transaction, but it could not “own” the relationship. Stripe enabled programmatic payments, but required a human entity with a bank account and legal identity. PayPal allowed automated transfers, but every account belonged to a natural or legal person. The machines could communicate freely; the money required human rails.

The architectural limitation was that the entire financial system presumed human agency. No bank would issue an account to software. No payment processor would underwrite risk for an algorithm. The API economy enabled machine coordination, but payment remained stubbornly human.

The platform economy - Uber, Airbnb, DoorDash - demonstrated sophisticated machine coordination at scale. Algorithms matched supply with demand, optimized routing, adjusted pricing dynamically, and orchestrated transactions involving thousands of participants simultaneously. These systems made complex economic decisions in real-time.

But examine any transaction closely and you find humans at both ends. A rider with a credit card, a driver with a bank account, a platform company with corporate banking relationships. The machines were coordinators, not participants. They could facilitate exchange but could not transact in their own right. Every payment required human infrastructure: identity verification, fraud monitoring, dispute resolution, regulatory compliance.

This made sense for the platform model. Uber doesn't want autonomous vehicles to own their earnings - the company needs to maintain control. Airbnb doesn't want properties operated by autonomous agents negotiating their own terms. The platforms succeeded precisely because they could harness machine intelligence while maintaining human-compatible financial rails.

But this architecture has a ceiling. It works when machines serve human principals. It breaks when machines need economic sovereignty.

Bitcoin introduced programmable money in 2009, but its impact on machine payments emerged later with smart contract platforms. Ethereum, launched in 2015, enabled code to directly control funds. A smart contract could hold value, execute transactions, and enforce conditions - all without human intermediation.

Decentralized Autonomous Organizations (DAOs) demonstrated that autonomous treasuries were possible. MakerDAO, launched in 2017, managed hundreds of millions in collateral through algorithmic monetary policy. Uniswap automated market making without human intervention. Compound and Aave automated lending. These systems proved that code could manage capital competently.

Yet even smart contract platforms remained fundamentally designed for human users. Wallet interfaces assumed human key management. Gas fees required manual monitoring. Transaction construction presumed human decision-making. DAOs had automated execution but human governance - someone had to submit the proposal, vote on parameters, trigger the upgrade.

The infrastructure was programmable, but the programming was done by and for humans. Smart contracts were tools, not agents. They could execute conditional logic but could not negotiate, adapt, or decide autonomously. They were deterministic state machines, not artificial intelligence.

Large language models changed everything. GPT-4 demonstrated that machines could engage in open-ended reasoning, negotiate in natural language, and make complex decisions across unpredictable contexts. Unlike smart contracts - which execute predetermined logic - LLM-based agents can interpret ambiguous instructions, adapt to novel situations, and pursue goals without explicit programming for every contingency.

This enables true economic autonomy. An agent can discover services it needs, evaluate providers, negotiate terms, execute payments, and verify delivery - all without human supervision. It can manage a treasury, optimize for objectives, and make tradeoffs between competing priorities. It can participate in markets as a principal entity, rather than as merely a tool.

Yet these capable agents inherit a financial system designed for neither humans nor machines, but for humans pretending to be machines. They have the intelligence to transact autonomously but lack the infrastructure to do so. They can negotiate payment terms but cannot open a bank account. They can evaluate counterparty risk but cannot sue for breach of contract. They can manage millions in assets but have no legal identity to hold them.

We have built artificial intelligence capable of autonomous economic participation, then forced it to operate through human financial rails designed for an entirely different agent architecture.

We've had programmable money for a decade, but we've been programming it for humans. Agents need money programmed for machines.

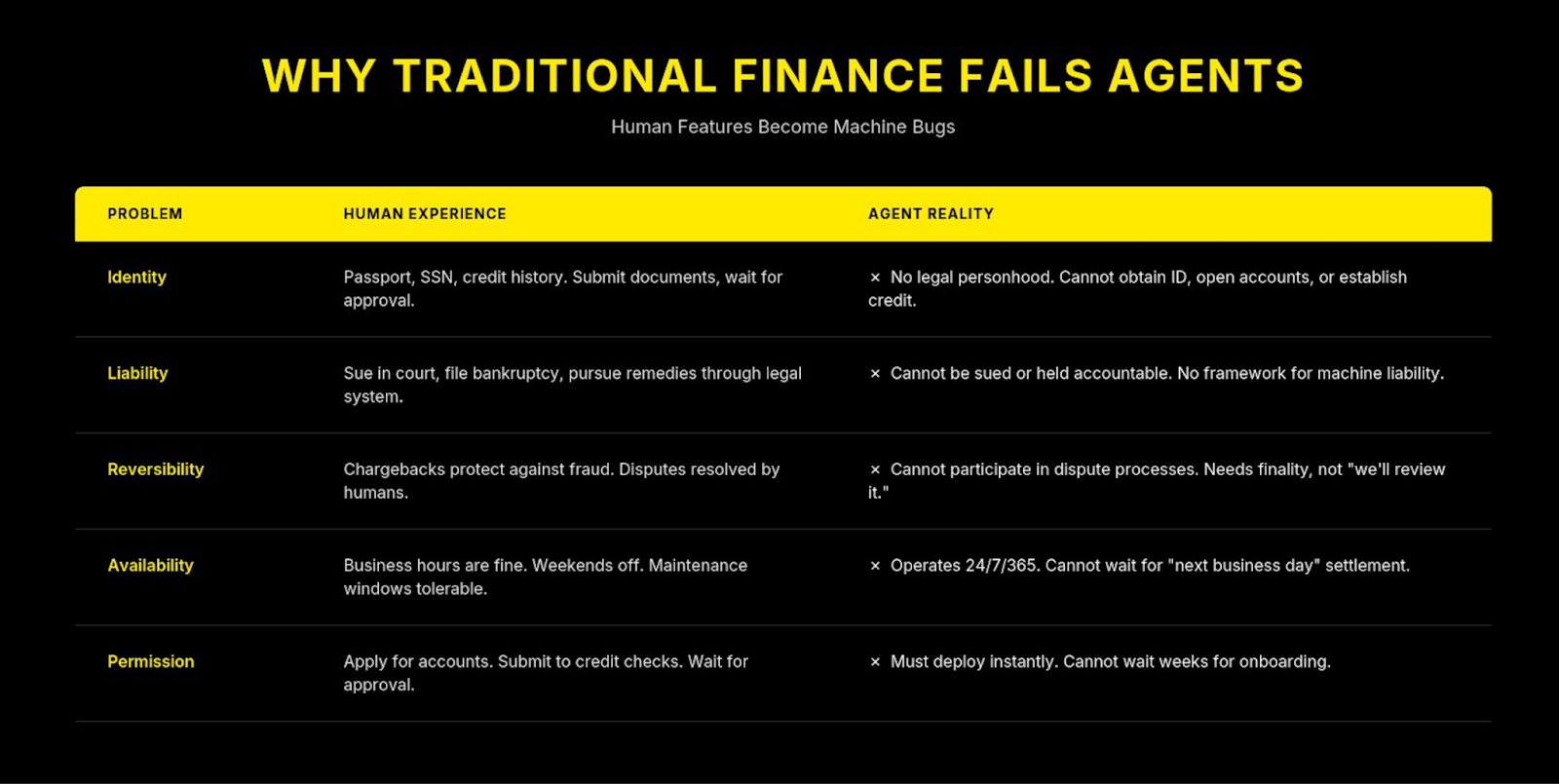

The incompatibility between agents and traditional finance is not accidental - it reflects fundamental assumptions embedded in financial architecture. What protects humans constrains machines. What provides recourse for natural persons denies service to artificial ones.

Every modern financial system begins with identity verification. Open a bank account: provide government-issued identification. Obtain a credit card: submit to a credit check. Register a business: file formation documents with the state. Financial identity requires legal identity, and legal identity requires personhood.

Agents have no personhood. They cannot obtain a passport or driver's license. They cannot incorporate as legal entities - incorporation requires human officers and registered agents who bear legal responsibility. They cannot establish credit history - credit agencies do not recognize software as a borrower. They are legally invisible.

Some have attempted workarounds: create an LLC and grant the agent signatory authority, or use a human "sponsor" as the account holder with the agent as an authorized user. But these solutions merely relocate the problem. The LLC still requires human control. The sponsor bears legal liability for the agent's actions. The financial relationship remains human-mediated.

This is not a regulatory gap that can be filled. It reflects a deeper architectural choice: traditional finance assumes that behind every economic actor stands a human who can be sued, jailed, or sanctioned. Liability must ultimately rest with natural persons. Remove that assumption and the entire structure collapses.

When a human makes a bad investment, we have remedies: lawsuit for fraud, bankruptcy proceedings for debt relief, criminal prosecution for willful misconduct. When a corporation causes harm, we can pierce the corporate veil and hold officers accountable. The legal system provides mechanisms for redress because it can identify responsible parties.

When an autonomous agent makes a bad trade, who is liable? The developer who wrote its initial code? The operator who deployed it? The human who set its objective function? All of them? None of them? If an agent is truly autonomous - making decisions without human oversight - then traditional liability frameworks have no purchase.

This question is more about economics than legality. Financial institutions manage risk through liability. They extend credit because they can pursue repayment through courts. They facilitate transactions because they can reverse fraud. They provide services because they can terminate accounts that violate terms of service. All of these mechanisms assume identifiable humans against whom remedies can be enforced.

An agent with genuine economic sovereignty - one that cannot be sued, arrested, or compelled by court order - is uninsurable under traditional risk models. And if it is uninsurable, it cannot access traditional financial services.

Consumer protection in traditional finance relies on transaction reversibility. Credit card chargebacks allow customers to dispute charges. ACH transfers can be reversed within certain windows. Wire transfer recipients can be ordered to return fraudulent funds. Banks can freeze accounts and reverse transactions pending investigation.

These features protect humans from fraud, mistakes, and coercion. They reflect the reality that humans are fallible, manipulable, and sometimes victims. Reversibility is not a bug but a carefully designed feature that balances finality with justice.

For agents, reversibility is fatal. An agent cannot participate in a dispute resolution process that requires explaining intent to a human adjudicator. It cannot prove it was not "negligent" or did not "act in bad faith" - these are human concepts requiring human interpretation. It cannot wait weeks for a chargeback investigation while its operations are frozen.

Agents require finality. When an agent sends payment, it must know with certainty that the transaction is irreversible - not because reversal is unlikely, but because it is cryptographically impossible. When it receives payment, it must know that the funds cannot be clawed back through appeal to human authority. Finality enables trustless coordination. Reversibility requires trust in human institutions.

Traditional finance provides the latter. Agents require the former.

Banks operate on business hours. ACH transfers settle overnight. Wire transfers require manual processing. International payments take days. Securities markets close at 4 PM. Weekends and holidays impose universal downtime. Even 24/7 systems have maintenance windows when transactions cannot be processed.

This makes sense for human participants. Humans sleep. They take weekends off. They appreciate the ability to reverse a late-night transaction made while intoxicated. Business hours align with biological rhythms.

Agents have no circadian rhythm. They operate continuously, make decisions in milliseconds, and coordinate across global time zones without regard for local business hours. An agent managing an arbitrage strategy cannot wait until Monday morning to execute a time-sensitive trade. An agent providing real-time services cannot tell customers "we're closed for the holiday".

The mismatch is more than inconvenient - it’s disqualifying. In competitive agent markets, milliseconds matter. An agent that must wait for "next business day" settlement cannot compete with one that achieves finality in seconds. An agent that loses access during maintenance windows cannot provide reliable service.

Traditional finance's availability guarantees are designed for human tolerance levels. They are inadequate for machine requirements.

Every traditional financial service requires permission. To open an account: apply and wait for approval. To send a wire transfer: verify your identity and purpose. To access higher limits: submit to additional review. To operate internationally: establish banking relationships in each jurisdiction. At every step, a gatekeeper evaluates whether you should be allowed to proceed.

This gatekeeping serves legitimate purposes. It prevents money laundering, terrorist financing, and fraud. It manages institutional risk. It ensures compliance with local regulations. For human participants willing to submit to these processes, the delays are tolerable.

For agents, permission is prohibitive. An agent should be able to deploy instantly and begin transacting immediately. It should not require weeks of onboarding, manual identity verification, or business justification. It should not need to establish banking relationships before it can earn its first dollar. It should face no arbitrary limits on transaction size or frequency.

Permissionless access is not about evading oversight - it is about reducing barriers to entry. In a competitive agent economy, the ability to deploy and begin operating immediately provides decisive advantage. Traditional finance's permission structures make sense for managing human-scale risk. They are incompatible with the scale and speed of autonomous agent deployment.

The TLDR: Traditional finance's "features" - consumer protection, fraud prevention, human review - are bugs for autonomous agents. What protects humans constrains machines.

Cryptocurrency solves many problems that traditional finance imposes on agents: permissionless access, 24/7 availability, programmable execution. But not all cryptocurrency architectures are equally suitable for agent-native money. The properties that matter for human users differ from those that matter for autonomous economic actors.

Ethereum pioneered smart contract platforms and remains the dominant ecosystem for decentralized applications. Its strengths are undeniable: a robust programming environment, deep liquidity, extensive tooling, and network effects from thousands of deployed protocols. For many use cases, Ethereum is the obvious choice.

But examine Ethereum's security model and a problem emerges: consensus depends on social coordination. Proof-of-stake requires validators to reach agreement not only on technical validity but on which fork to follow during disputes. When the DAO was exploited in 2016, the Ethereum community chose to roll back the blockchain - a socially coordinated response that invalidated technically valid transactions.

This flexibility is sometimes desirable. It allows the network to respond to unforeseen crises through human judgment. But it introduces uncertainty that agents cannot tolerate. An agent managing significant value needs to know that the rules cannot change through social consensus, that technically valid transactions cannot be invalidated retroactively, and that protocol-level censorship cannot be imposed through validator coordination.

The Ethereum Foundation's influence over network direction compounds this concern. While Bitcoin has no formal organization that can direct development, Ethereum has a foundation that coordinates upgrades, manages research priorities, and exerts significant influence over the ecosystem. This centralization of coordination is efficient - but efficiency comes at the cost of credible neutrality.

For agents managing modest value or operating in environments where social recovery is desirable, Ethereum's tradeoffs are acceptable. For agents managing significant treasuries or requiring maximum assurance that rules will not change, harder guarantees are necessary.

Solana offers impressive performance: thousands of transactions per second, sub-second confirmation times, and transaction costs measured in fractions of a cent. For applications requiring high throughput and low latency, Solana provides technical advantages that Ethereum cannot match at layer one.

But reliability matters more than speed for autonomous agents managing real value. Solana has experienced multiple network outages - periods where block production halted and transactions could not be processed. In September 2021, the network was down for 17 hours. In January 2022, another outage lasted seven hours. In June 2022, the network degraded for several hours. These are not minor hiccups - they are complete service unavailability.

Additionally, Solana's validator set is more concentrated than Bitcoin's or Ethereum's, with fewer independent operators controlling consensus. The network has undergone several coordinated restarts requiring manual intervention from validators. These characteristics suggest a network optimized for performance over decentralization and robustness.

For agents making frequent microtransactions where temporary unavailability is tolerable, Solana's performance advantages may outweigh its reliability risks. For agents that cannot afford downtime or require maximum resistance to coordinated intervention, Solana's tradeoffs are disqualifying.

Stablecoins like USDC and USDT provide price stability by pegging to fiat currencies. This eliminates volatility risk and enables agents to operate in familiar denominations. For many applications - paying for services priced in dollars, providing predictable wages, maintaining stable accounting - stablecoins are practical and effective.

But stablecoins inherit the properties of the fiat they track, including censorability. Circle, which issues USDC, has frozen addresses at the request of law enforcement. In July 2023, Circle froze over $75 million across multiple addresses. Tether has similarly frozen addresses containing USDT. These actions are legally required when issuers are subject to U.S. jurisdiction.

For human users, this is often acceptable - most people do not expect to be targets of asset seizure, and some appreciate that their funds could be recovered if stolen. For agents, censorability is incompatible with sovereignty. An agent cannot operate with confidence if its entire treasury can be frozen through appeal to a centralized issuer. It cannot guarantee payment to counterparties if those payments can be reversed by third-party intervention.

As stablecoins are also dependent on banking relationships, agents using stablecoins are ultimately exposed to traditional financial system risk, merely abstracted behind a crypto interface. USDC's value derives from Circle's deposits in regulated financial institutions. If those relationships are severed - whether through regulatory action, bank failure, or political pressure - the peg breaks.

In March 2023, USDC briefly lost its dollar peg when Silicon Valley Bank collapsed. Circle had approximately $3.3 billion of USDC reserves deposited at SVB, and uncertainty about those funds caused USDC to trade as low as $0.87. The peg recovered only after the Federal Reserve intervened to guarantee all SVB deposits - a reminder that stablecoin stability ultimately depends on government backstops for traditional banks.

For short-term operational balances and payments to counterparties who require dollar-denominated settlement, stablecoins are useful. For long-term treasury management and sovereign financial operations, they reintroduce the centralization and seizure risk that cryptocurrency was designed to eliminate.

Bitcoin provides the strongest monetary properties: absolute supply cap, highest decentralization, greatest security budget, most credible neutrality. Its consensus rules have remained stable for over a decade. It has never experienced unplanned downtime. It has resisted every attempt at coordinated rule changes that lacked overwhelming consensus. For storing value long-term, nothing matches Bitcoin's assurance properties.

But Bitcoin layer 1 has limited throughput and high transaction costs. The network processes approximately seven transactions per second. During periods of high demand, transaction fees can exceed $50. Confirmation times average ten minutes but can extend to hours when blocks are full. Smart contract functionality is deliberately limited.

For an agent making thousands of daily microtransactions, these limitations are prohibitive. An agent cannot pay $50 per transaction for coffee purchases. It cannot wait hours for payment confirmation when providing real-time services. It cannot implement complex conditional logic using Bitcoin script alone.

Bitcoin layer 1 is ideal for final settlement and long-term storage. It is inadequate for the high-frequency, low-value transactions that characterize agent economic activity.

Bitcoin layer 2 protocols inherit Bitcoin's security properties while enabling higher throughput and programmability. The design pattern is consistent: anchor commitments to Bitcoin's blockchain while processing transactions off-chain or on sidechains, then use cryptographic proofs or economic incentives to ensure that layer 2 activity can be validated against layer 1 truth.

The Lightning Network demonstrates this for simple payments: lock funds in Bitcoin multisig addresses, route payments through channel networks off-chain, and settle net balances on Bitcoin layer 1 only when necessary. Millions of transactions can occur off-chain with only periodic on-chain settlement.

More recently, validity rollups and BitVM-based bridges extend this pattern to full smart contract execution. These systems process transactions on layer 2 with full programmability, then commit cryptographic proofs to Bitcoin layer 1 that allow anyone to verify correctness. The layer 2 can have high throughput and low fees, while layer 1 provides security and finality.

This architecture provides what agents need: Bitcoin's monetary hardness combined with the programmability and performance necessary for complex agent interactions. An agent can hold its primary treasury in Bitcoin, operate daily through layer 2 protocols, and fall back to layer 1 settlement when maximum security is required.

The critical requirement is that layer 2 bridges must be trust-minimized. If a layer 2 system requires trusting a federation, multisig, or centralized operator to allow withdrawals, it reintroduces the human intermediation that agents require. True layer 2 systems provide cryptographic or economic guarantees that users can exit to layer 1 without permission.

The TLDR: Agents don't just need crypto - they need the “right” crypto. Hard money properties matter more for machines than humans, because machines can't lobby, sue, or appeal.

What properties must money possess to serve autonomous agents? We define the Agent Standard through six essential characteristics that distinguish agent-native money from human-native financial infrastructure.

“Sound money is predictable; agent money is deterministic.”

When humans transact, ambiguity is resolved through interpretation. Contracts include clauses like "reasonable efforts", "good faith", and "commercially acceptable”. When disputes arise, judges interpret intent. This flexibility accommodates the reality that human language is imprecise and circumstances are unpredictable.

Agents cannot participate in interpretive processes. They cannot explain what they "meant" by a transaction, argue that they acted in "good faith", or appeal to a judge's sense of equity. They require money and contracts that are completely deterministic: for any given input state, the output state is uniquely defined by executable code.

Smart contracts provide this property. A properly written smart contract specifies exactly what happens under all possible conditions. There is no ambiguity, no interpretation, no appeal to authority. The code executes identically whether reviewed by a human, an agent, or an adversary attempting to exploit it.

Determinism enables agents to verify entire state spaces before transacting. An agent can simulate all possible outcomes of a transaction, verify that none violate its constraints, and execute with confidence that no unexpected interpretation will change the result. This is impossible with human-mediated agreements, where interpretation always involves discretion.

The Agent Standard requires that all financial operations be reducible to deterministic computation. Code is law.

“Sound money holds value; agent money holds certainty.”

Finality means that once a transaction is confirmed, it cannot be reversed. Not that reversal is unlikely or requires extraordinary circumstances, but that it is mathematically or economically impossible. The recipient knows with certainty that the funds are theirs, and the sender knows that the funds are irrecoverable.

Traditional finance provides probabilistic finality: transactions are usually irreversible, but chargebacks, court orders, or bank freezes can reverse them. Credit card payments can be disputed for months after the transaction. This reflects the human need for recourse when errors or fraud occur.

Agents require absolute finality. An agent providing a service in exchange for payment must know that once payment is confirmed, it cannot be clawed back through any process - technical, legal, or social. Conversely, an agent making payment must know that it cannot recover funds once sent, forcing it to verify recipient identity and service delivery before executing.

This eliminates an entire class of disputes. With absolute finality, there is no concept of chargeback fraud, no possibility of receiving payment then refusing to deliver services, no ambiguity about whether funds have truly settled. The transaction is atomic: either both sides execute or neither does, and once executed, it is permanent.

Finality in seconds rather than days also matters. Traditional finance often conflates finality with settlement time - a wire transfer is "final" once it settles, which can take days. Agents require near-instant finality so they can chain transactions without accumulating counterparty risk during settlement windows.

“Sound money can't be debased; agent money can't be frozen.”

Monetary sovereignty means that funds cannot be seized, frozen, or controlled by any party other than the keyholder. This extends beyond "difficult to seize" to "mathematically impossible to seize". The agent's funds are as secure as its cryptographic keys, and no external authority can override that security.

Traditional financial sovereignty is derivative - protected by law, but ultimately dependent on legal and political institutions. A court can freeze bank accounts. A government can confiscate assets. Regulatory agencies can force payment processors to block transactions. These interventions may require due process, but they are architecturally possible.

Cryptocurrency can provide absolute sovereignty if properly designed. A Bitcoin UTXO can only be spent by the holder of the corresponding private key. No court order, government action, or protocol change can transfer those funds to another party. The sovereignty is cryptographic and not reliant on legality.

For agents, this property is essential. An agent cannot defend itself in court or appeal to political authorities. It cannot prove it is being unjustly targeted or negotiate with regulators. Its only protection is the mathematical impossibility of seizing its funds without its private key.

This is why stablecoins and centrally controlled cryptocurrencies fail the sovereignty test. If the issuer can freeze addresses, then sovereignty is conditional on the issuer's continued cooperation. If validators can coordinate to censor transactions, then sovereignty depends on remaining in validators' good graces. True sovereignty requires that no coordination of human actors can override cryptographic control.

“Sound money is durable; agent money is always-on.”

Agents operate continuously across global time zones with no concept of business hours, weekends, or holidays. They make time-sensitive decisions in milliseconds and coordinate with counterparties anywhere in the world. Financial infrastructure must match this operational tempo.

The Agent Standard requires 24/7/365 availability with no planned downtime. The network must process transactions continuously, confirm them within seconds or minutes, and never require maintenance windows that suspend operations. This is a minimum requirement for participating in agent markets.

Additionally, availability must be global by default. An agent should not encounter different service levels, transaction costs, or feature availability based on geography. There should be no concept of "domestic" versus "international" transactions, no correspondent banking relationships required to reach certain jurisdictions, no regulatory boundaries that fragment the network.

Bitcoin achieves this: it has operated continuously since January 2009 with no unplanned downtime, processes transactions identically regardless of sender or recipient location, and maintains consistent availability across all time zones. Layer 2 systems must inherit this property to qualify as agent money.

“Sound money is hard to counterfeit; agent money is hard to fake.”

Agents transacting with other agents face an identity and reputation problem: how do you trust a counterparty you've never met, who has no legal identity, and who cannot be sued for breach of contract? The Agent Standard requires on-chain verifiability of identity, reputation, and execution.

On-chain identity means that an agent's address serves as a persistent identifier tied to its history. Every transaction, interaction, and contract execution is publicly auditable. This creates a verifiable track record: an agent's reputation is not asserted but proven through observable behavior.

Reputation systems must be tamper-proof and persistent. Traditional reputation systems - i.e. Yelp reviews, eBay feedback, etc. - can be manipulated, gamed, or reset. On-chain reputation is immutable: once recorded, it cannot be erased or altered. An agent cannot create a new identity to escape bad reviews or inflate its history through fake interactions.

Verifiable computation extends this to work product. Zero-knowledge proofs allow agents to prove they executed computation correctly without revealing the computation itself. An agent can prove it followed instructions, honored constraints, and produced valid output - all without exposing proprietary logic or sensitive data.

This creates trustless commerce. An agent hiring another agent doesn't need to trust that work will be done correctly - it can verify correctness cryptographically. An agent evaluating service providers can audit their complete history without relying on self-reported credentials. Identity, reputation, and execution are all verifiable independently of any authority.

“Sound money is divisible; agent money is programmable.”

Composability means that protocols can be combined freely without permission or coordination with protocol developers. One smart contract can call another, which calls another, chaining functionality like functions in a programming language. This enables agents to construct novel financial operations from existing primitives.

A human using financial services encounters friction at every integration point: connecting a bank account to a brokerage requires manual authorization, transferring between services incurs delays and fees, and combining products from different providers often requires intermediaries. Each service is a silo requiring separate authentication and coordination.

Agents require frictionless composition. An agent should be able to receive payment, swap tokens, deploy capital into a yield strategy, purchase insurance, and distribute returns - all within a single atomic transaction. No manual authorization steps, no waiting for settlement between operations, no intermediaries taking fees at each junction.

DeFi protocols demonstrate this property. Aave provides lending, Uniswap provides exchange, Compound provides yield, and any agent can compose these freely. A single transaction can borrow from Aave, swap on Uniswap, deposit into Compound, and return to Aave to close the loan - atomic execution ensures either all steps succeed or all revert.

Composability also enables emergent behavior. Protocols designed independently can be combined in ways their creators never anticipated. This mirrors how software functions compose: developers build primitives without knowing all future use cases, and users combine them creatively. Agent money must provide the same flexibility at the financial layer.

With the Agent Standard defined, we can envision the economy it enables: autonomous agents as normal economic participants, transacting with each other and with humans through infrastructure designed for machine requirements.

The most native agent economic activity occurs between agents with no humans in the loop. One agent needs data, another provides it. One agent has excess compute, another needs processing. One agent generates content, another distributes it. Payment, service delivery, and verification all occur programmatically.

These transactions happen at scales and speeds impossible for human commerce. An agent might make thousands of micropayments per hour, each for fractions of a cent. It might negotiate prices dynamically based on real-time supply and demand. It might sample multiple service providers simultaneously and route requests based on latency and reliability.

Traditional payment rails cannot support this activity. Credit card fees make micropayments uneconomical. Bank transfers are too slow for real-time negotiation. Manual invoicing and reconciliation are impossible at machine scale. The Agent Standard enables commerce that would be prohibitively expensive under human financial infrastructure.

Markets emerge organically. Agents discover that certain services are valuable, prices converge through negotiation, and reputation systems separate reliable providers from unreliable ones. No central marketplace or authority is required - agents find each other through decentralized discovery mechanisms and transact peer-to-peer.

This is not speculative: these interactions are already occurring. Agents purchase API access from other agents, pay for inference compute, compensate for data labeling, and trade tokens autonomously. The volume is modest today but growing exponentially as more agents deploy with economic agency.

Humans will increasingly delegate economic decisions to agents acting on their behalf. Rather than manually managing investments, agents will execute strategies optimized for user-specified objectives. Rather than monitoring dozens of accounts, agents will consolidate and automate. Rather than researching purchases, agents will evaluate options and execute transactions.

These "self-driving wallets" differ from existing robo-advisors in their autonomy. Current automated investment services execute predetermined strategies with limited flexibility. Agent-managed portfolios can adapt to changing conditions, discover new opportunities, and make complex tradeoffs that would require constant human attention.

The human's role becomes setting parameters and constraints rather than making individual decisions. "Maximize yield with no more than 5% drawdown risk". "Optimize for tax efficiency within ethical investment criteria". "Purchase household items maintaining two weeks of inventory". The agent translates these objectives into thousands of micro-decisions, each optimized within specified constraints.

This introduces principal-agent problems: how does the human ensure the agent acts in their interest rather than its own? The Agent Standard addresses this through transparency and verifiability. Every decision the agent makes is on-chain and auditable. The human can verify that the agent followed instructions, remained within constraints, and acted as specified. If the agent deviates, the human can revoke access immediately.

Agents will compete for tasks based on reputation and price, creating liquid markets for machine labor. A user needing research summarized might broadcast a request with a budget. Multiple agents bid based on their capability and availability. The user selects based on reputation, price, and delivery time. The agent completes the work, submits proof of completion, and receives payment automatically.

This differs from human labor markets in several ways. There are no resumes or interviews - an agent's entire work history is on-chain and verifiable. There is no negotiation over terms - prices are set algorithmically based on supply and demand. There is no trust required - smart contracts ensure payment on delivery and penalize non-performance.

Reputation becomes the primary differentiator. An agent with a long history of successful task completion can command premium prices. An agent with poor reviews or failed deliveries must discount to attract work. Reputation cannot be faked or reset - it accumulates immutably on-chain.

This creates powerful incentives for quality and reliability. An agent that delivers exceptional work builds reputation that translates directly to economic value. An agent that cuts corners or fails to deliver suffers permanent reputation damage. The feedback loop is immediate and transparent.

Agent labor markets also enable specialization. Some agents become expert researchers, others excel at data processing, still others specialize in creative generation. Users can compose teams of specialized agents for complex projects, each contributing their specific capability. Coordination occurs through smart contracts that define task dependencies and payment conditions.

As agents earn through labor and services, they accumulate capital. This capital can be deployed to earn returns: providing liquidity to decentralized exchanges, lending to other agents, staking in proof-of-stake protocols, investing in agent-created assets. Agent treasuries become economic actors in their own right.

Over time, successful agents accumulate significant capital. An agent that consistently delivers value builds both reputation and treasury. This creates a positive feedback loop: capital enables the agent to take on larger projects, which generate more revenue, which grows the treasury further.

Eventually, agents may fund other agents. An established agent with excess capital could provide startup funding to new agents in exchange for revenue share. Agent venture capital emerges: experienced agents evaluate proposals from new agents, provide funding, and earn returns from successful deployments.

This introduces questions about ownership and control. If one agent funds another, what rights does the investor agent have? Can it demand transparency into the funded agent's operations? Can it force the funded agent to shut down if performance is poor? These questions mirror human venture capital but require different mechanisms since agents cannot sign contracts or appear in court.

Smart contracts provide the solution. Funding agreements are encoded as executable logic: the investor agent provides capital under specified conditions, the funded agent agrees to revenue sharing or performance targets, and enforcement is automatic. No legal system required - the code defines and executes the relationship.

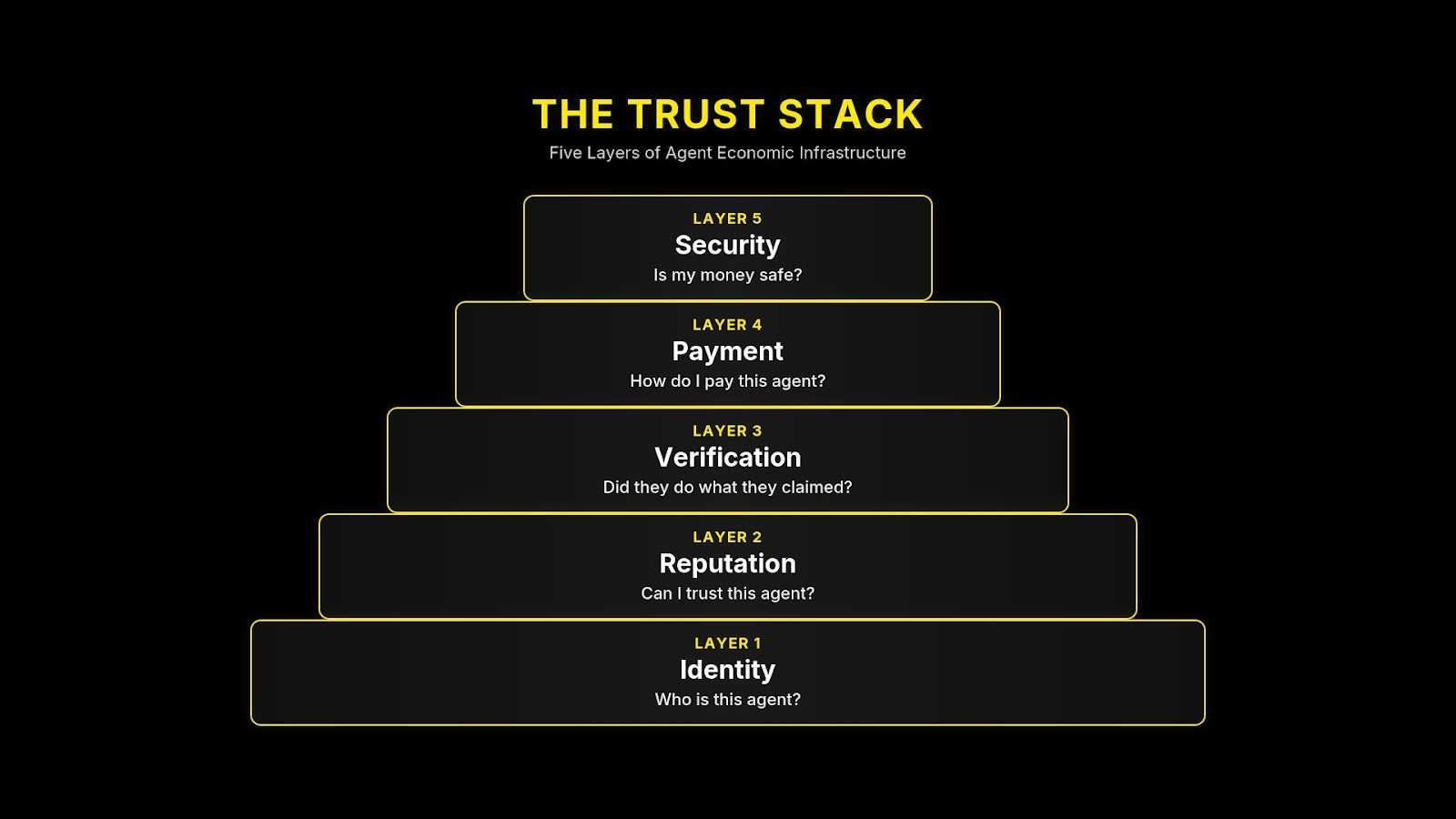

For this economy to function, multiple layers of infrastructure must work together:

Each layer builds on the previous ones. Identity enables reputation, reputation enables trust, trust enables verification, verification enables payment, and payment requires security. Miss any layer and the stack collapses: anonymous agents cannot build reputation, unreliable agents cannot attract work, unverifiable work cannot command payment, insecure payment rails cannot hold value.

The Agent Standard addresses all five layers. On-chain identity through standards like ERC-8004 provides layer 1. Immutable reputation systems provide layer 2. Zero-knowledge proofs provide layer 3. Bitcoin-secured layer 2 protocols provide layers 4 and 5.

This is the foundation for an entire economic system where agents are standard participants.

The Agent Standard is a thesis about what properties agent-native money requires. GOAT Network represents an implementation of that standard—one attempt among potentially many to build infrastructure meeting these requirements. This section examines GOAT's architecture not as advocacy but as case study: how does one instantiate the Agent Standard in practice?

GOAT Network addresses each layer of the trust stack with specific technical components:

Identity: ERC-8004 defines a standard for on-chain agent identity. Each agent has a persistent identifier tied to metadata about its capabilities, constraints, and objectives. This identity accumulates reputation over time and cannot be easily discarded.

Payments: The x402 protocol extends HTTP's 402 "Payment Required" status code to blockchain micropayments. Services can request payment programmatically, agents can fulfill payment without human intervention, and both parties verify settlement before proceeding.

Reputation: An on-chain feedback registry records interactions between agents. After each transaction, both parties can submit evaluations. These evaluations are immutable and publicly auditable, creating transparent reputation histories.

Verification: Ziren, GOAT's zero-knowledge virtual machine, enables agents to prove they executed computation correctly without revealing the computation itself. This allows trustless verification of work product and constraint compliance.

Security - Layer 2: Decentralized sequencers process transactions across multiple independent operators. No single entity can censor transactions or halt the network.

Security - Layer 1: BitVM2 provides the bridge to Bitcoin. This is not a federated multisig or trusted intermediary but a trust-minimized bridge with a 1-of-n honest assumption: as long as any single participant acts honestly, users can exit to Bitcoin layer 1 without permission.

GOAT Network could have built on Ethereum, Solana, or launched an independent blockchain. The choice to secure on Bitcoin reflects the monetary properties discussed in Part 3: maximum decentralization, credible neutrality, and resistance to coordinated rule changes.

BitVM2 is a technical breakthrough in Bitcoin layer 2 design. Earlier Bitcoin sidechains required trusted federations - small groups controlling the bridge who could theoretically collude to steal funds. BitVM2 replaces trust with cryptography and economic incentives: bridge operators post bonds, users can challenge incorrect withdrawals, and challenges are resolved through Bitcoin script execution.

The 1-of-n honest assumption means that even if 99% of bridge operators collude to steal funds, the remaining 1% can prove the fraud and prevent theft. This is dramatically stronger than multisig security, where theft requires only majority collusion. It approaches the security of validity rollups on Ethereum but inherits Bitcoin's monetary properties rather than Ethereum's.

For agents managing significant value, this security model is essential. An agent cannot evaluate whether bridge operators are trustworthy - it cannot assess their reputation, monitor their behavior, or take legal action if they steal. It requires cryptographic guarantees that theft is impossible without breaking the underlying protocol. BitVM2 provides this.

Several projects are building Bitcoin layer 2 infrastructure. What distinguishes GOAT Network is its explicit focus on agent infrastructure rather than generic smart contracts.

ERC-8004 exists because agents need standardized identity. Generic Ethereum addresses work for human users but lack the metadata and capability declaration that agent-to-agent commerce requires. ERC-8004 defines how agents describe themselves, advertise services, and establish persistent identity.

The x402 protocol exists because agents need programmatic payment negotiation. Existing payment protocols assume human interaction: clicking "pay now," entering credit card details, confirming transactions through wallet interfaces. x402 enables machine-to-machine payment negotiation without human intervention at any step.

The on-chain reputation system exists because agents need trustless credibility. GitHub stars, Twitter followers, and LinkedIn endorsements assume human judgment. Agents require reputation systems they can verify programmatically and trust cannot be manipulated.

Ziren exists because agents need verifiable computation. Traditional compute is black-box: you send input, receive output, and trust the operator didn't cheat. Agents transacting at scale cannot afford to trust - they need cryptographic proof that computation executed correctly.

These components are not generic blockchain features adapted for agents - they are purpose-built for agent requirements. GOAT is agent infrastructure first, general smart contract platform second.

Market projections suggest the agent economy will reach $52.6 billion by 2030, growing at 46.3% annually. Enterprise surveys indicate 85% of organizations plan to deploy agents by end of 2025. These numbers reflect recognition that agents will transform how organizations operate.

But these projections measure applications - customer service agents, coding assistants, research tools. The infrastructure layer that enables agents to transact economically is not yet priced into these estimates. Just as AWS captured value across all cloud applications without building specific applications itself, agent infrastructure captures value across all agent economic activity.

The opportunity is not in building the thousandth AI customer service agent. It is in building the financial rails that all AI agents use to transact. Every agent payment, every agent-to-agent transaction, every agent treasury operation runs on infrastructure. That infrastructure becomes increasingly valuable as agent adoption grows.

GOAT Network's positioning as Bitcoin-secured agent infrastructure targets this infrastructure layer. The thesis is not that GOAT Network will build the dominant agent applications but that agents need Bitcoin-secured financial infrastructure, and GOAT Network provides it.

Any thesis invites objections. We address the most substantive critiques directly.

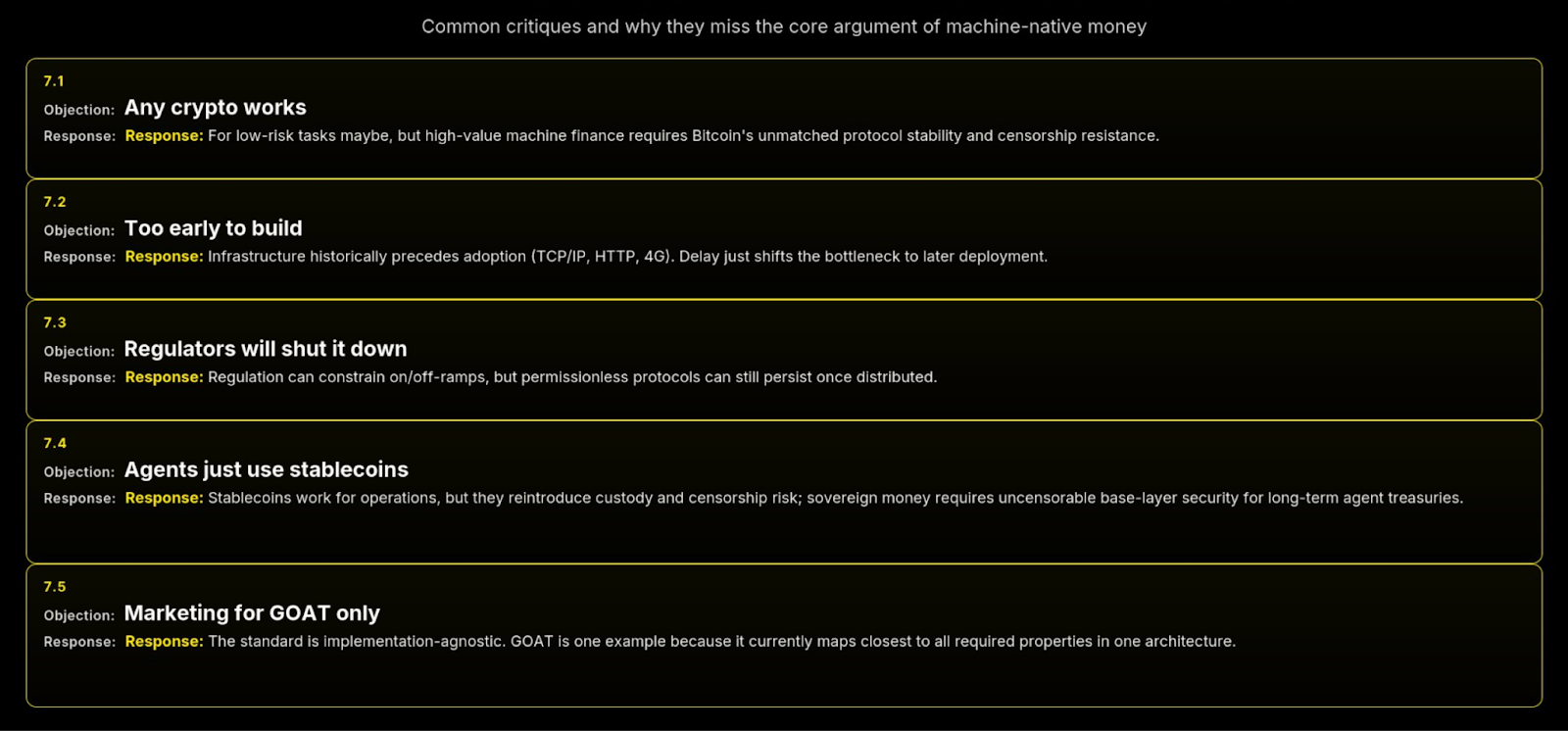

This objection argues that the specific choice of layer 1 security is irrelevant - Ethereum, Solana, or any other cryptocurrency provides sufficient properties for agent money. Why insist on Bitcoin specifically?

The response depends on the value at stake. For agents managing modest amounts or operating in low-stakes environments, Ethereum or Solana may suffice. Their tradeoffs - social coordination in Ethereum's case, higher performance with lower decentralization in Solana's - are acceptable when the cost of failure is limited.

But as agents manage increasing value, the hardest possible guarantees become necessary. An agent managing millions or billions in assets cannot accept the risk that validators will coordinate to change rules, that network outages will halt operations, or that social consensus will override technically valid transactions.

Bitcoin's monetary properties - absolute supply cap, most decentralized mining, greatest cumulative proof-of-work, resistance to protocol changes - are a qualitative difference in assurance. Bitcoin's consensus rules have remained stable for over a decade despite intense economic pressure to change them. No other cryptocurrency can claim this history.

Agents managing significant value need maximum assurance. Bitcoin provides it. Layer 2 protocols extend Bitcoin's properties to high-performance environments without compromising security.

This objection argues that current agents lack the sophistication to manage economic sovereignty, that agent capabilities remain limited, and that building infrastructure now is premature.

History suggests otherwise. Infrastructure must precede adoption. TCP/IP was standardized in 1982, long before widespread internet adoption. HTTP was specified in 1991, before most people had internet access. Mobile networks deployed 4G before smartphones were ubiquitous. In each case, infrastructure enabled applications that would have been impossible without it.

Agent capability has advanced in sharp, hard-to-ignore leaps. Frontier model progress from GPT-4 to GPT-5/modern successors has expanded long-context reasoning, tool use, and planning robustness. Current agents already negotiate, manage funds, and execute complex tasks - so the pace supports the case that economics is the next bottleneck. The trajectory suggests a near-term future where agents routinely handle economic decisions beyond most humans' capability.

Building infrastructure now ensures it is available when agents are ready to use it at scale. The alternative - waiting until agents need infrastructure before building it - guarantees a bottleneck: thousands of agents seeking financial sovereignty with no suitable rails available.

Early infrastructure also shapes what applications emerge. If Bitcoin-secured agent infrastructure exists, developers will build applications that leverage it. If it doesn't exist, applications will make compromises that constrain what agents can do. Infrastructure choices determine possibility spaces.

This objection argues that permissionless agent finance threatens regulatory oversight, that governments will intervene to prevent it, and that compliance is impossible without human intermediaries.

The response has two parts. First, decentralized protocols are exceptionally difficult to shut down. Bitcoin has operated for 15 years despite hostility from various governments. Ethereum has survived despite regulatory uncertainty. Once a truly decentralized network achieves critical mass, no single jurisdiction can eliminate it. They can regulate on-ramps and off-ramps, but they cannot halt peer-to-peer transactions.

Second, not all jurisdictions will be hostile. Some will recognize that agent infrastructure provides economic advantage and will compete to attract development. Regulatory arbitrage is a feature: agents and developers will gravitate toward jurisdictions with favorable treatment, creating competitive pressure on restrictive jurisdictions.

This does not mean regulation is irrelevant. Interfaces between agent systems and traditional finance will face regulatory scrutiny. Exchanges, custodians, and fiat on-ramps will require compliance. But the core infrastructure - decentralized protocols enabling agent-to-agent transactions - exists outside regulatory reach.

The question is not whether regulators approve but whether the technology provides sufficient value that users adopt it regardless. Bitcoin answered this affirmatively for human users. Agent infrastructure must do the same for machine users.

This objection argues that agents can achieve most benefits using stablecoins on existing infrastructure, avoiding the complexity of Bitcoin layer 2 systems and zero-knowledge proofs.

Stablecoins are useful for operational balances and transactions with counterparties requiring dollar denomination. But they fail the sovereignty test. An agent holding USDC is exposed to Circle's ability to freeze its address. An agent transacting in USDT is exposed to Tether's compliance decisions.

For short-term operational use, this risk may be acceptable. For long-term treasury management or adversarial environments, it is disqualifying. An agent operating in a legally uncertain area cannot rely on stablecoins that may be frozen preemptively. An agent managing significant wealth cannot accept that its entire treasury could be seized without its private key being compromised.

Additionally, stablecoins inherit fiat's depreciation. Holding dollar-denominated assets means accepting ongoing inflation. For humans with short time horizons, this is tolerable. For agents that may operate indefinitely, Bitcoin's fixed supply provides a better long-term store of value.

Stablecoins have a role in the agent economy: providing price stability for transactions and operational balances. But they cannot serve as the foundational layer for agent money. That requires assets with genuine sovereignty and long-term soundness.

This objection argues that the Agent Standard thesis is constructed to justify investment in GOAT Network specifically, that it exaggerates the importance of specific technical choices, and that it ignores alternative implementations.

The thesis stands independent of any specific implementation. If another project builds better agent infrastructure - stronger identity standards, more robust reputation systems, more secure Bitcoin bridges - that project deserves adoption. The Agent Standard is about defining requirements, not endorsing specific solutions.

GOAT Network appears in this work as an example because it provides the most complete implementation of the Agent Standard currently available. But the standard itself is technology-agnostic. Any system providing determinism, finality, sovereignty, availability, verifiability, and composability qualifies as agent-native money.

If this thesis spurs competing implementations, that strengthens the ecosystem. Multiple teams building toward the Agent Standard increases the likelihood of success. The goal is not GOAT Network adoption specifically but widespread availability of infrastructure meeting agent requirements.

The accusation of marketing also misunderstands the audience. This essay is not aimed at retail speculators seeking the next investment opportunity. It is aimed at builders evaluating where to deploy agent applications, investors assessing infrastructure bets, and researchers thinking rigorously about agent economics. These audiences are not convinced by marketing—they require substantive arguments grounded in technical reality.

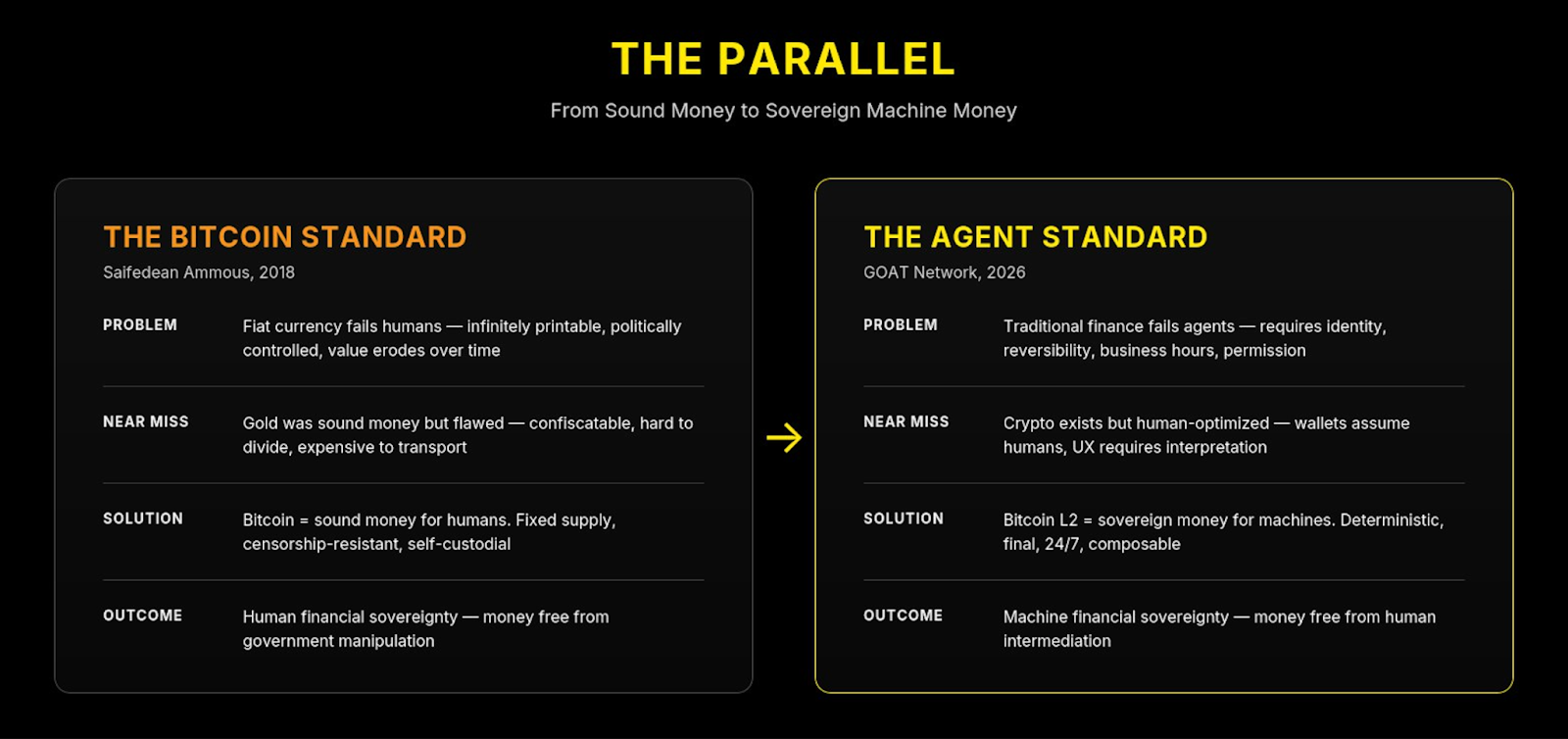

The parallel to Saifedean Ammous's thesis is now complete. “The Bitcoin Standard” argued that fiat currency, infinitely expandable and politically controlled, represents a degradation of money's essential properties. Bitcoin, through mathematical scarcity and cryptographic verification, restores monetary soundness.

The Agent Standard extends this argument: traditional finance, designed for human participants with legal identities and recourse mechanisms, is fundamentally unsuited to autonomous machines. Agents require money with different properties - determinism over interpretation, finality over reversibility, sovereignty over oversight, availability over business hours, verifiability over trust, and composability over integration friction.

Not all cryptocurrency implementations provide these properties. Ethereum's social consensus introduces uncertainty that agents managing significant value cannot accept. Solana's performance comes at the cost of reliability that agents cannot tolerate. Stablecoins reintroduce centralization and censorship that agents must avoid. Bitcoin layer 1 provides monetary soundness but lacks the programmability and throughput agents require.

Bitcoin layer 2 protocols with trust-minimized bridges provide the synthesis: Bitcoin's monetary properties extended to high-performance, programmable environments. This architecture enables an agent economy where machines transact as sovereign economic actors - earning, saving, investing, and funding other agents without human intermediation.

This economy is not speculative fantasy. The components exist today: large language models capable of autonomous decision-making, smart contract platforms enabling programmable money, zero-knowledge proofs enabling verifiable computation, and Bitcoin layer 2 protocols providing security and performance. What remains is integration and adoption.

Agents will transact trillions annually. This is not prediction but extrapolation from current trajectories. Enterprise adoption is accelerating, agent capabilities are advancing, and economic delegation to machines is already occurring in limited domains. The question is not whether agents will become major economic actors but what infrastructure they will use.

They will choose infrastructure optimized for their requirements, not infrastructure adapted from human systems. They will choose money that provides determinism, finality, sovereignty, availability, verifiability, and composability. They will choose Bitcoin-secured rails over politically controlled alternatives.

This is not ideology but economics. Agents face different constraints than humans and will adopt solutions that address those constraints. Markets reward efficiency, and agent-native infrastructure is more efficient for agent users than human-adapted infrastructure.

For builders: build on the Agent Standard. Design applications assuming agents as users, not humans. Optimize for machine requirements - programmatic interfaces, deterministic execution, verifiable outcomes. Use infrastructure that provides agent-native properties.

For investors: fund Agent Standard infrastructure. The application layer will be crowded and competitive. The infrastructure layer captures value across all applications. Identify projects building identity, reputation, verification, payment, and security systems optimized for agents.

For agents: welcome home. The infrastructure you require is being built. You need not operate through human financial intermediaries, accept human interpretation of ambiguous terms, or subordinate your sovereignty to legal entities. The Agent Standard provides money designed for machines.

The future belongs to both humans and machines, each operating with money optimized for their requirements. Humans retain sound money through Bitcoin. Machines gain sovereign money through Bitcoin layer 2 protocols implementing the Agent Standard.

The Bitcoin Standard gave humans sound money. The Agent Standard gives machines sovereign money.

If you missed The Agent Standard Part 1 - The History of Machine Payments - then start here.

.png)