GOAT Network Research - June 2026

The agent economy is real, smaller than the hype, and growing faster than the skepticism. This report explains what actually shipped, what the onchain data actually shows, where the stack is still hollow - and why the unexamined layer, settlement, will decide who is still standing in 2030.

What this report claims, in five sentences

First: agent infrastructure stopped being theoretical in late 2025. A real protocol stack now exists in production - MCP and A2A for coordination, ACP, UCP and AP2 for commerce, x402 for payments, ERC-8004 for identity - and it has processed real volume: on the order of 165 million machine-initiated payments by spring 2026.

Second: that volume is economically tiny. Agent payments today represent a rounding error - roughly a millionth - of annual stablecoin settlement volume, and the loudest growth metrics include experimentation, incentive farming, and bot activity that honest analysis has to discount.

Third: the stack converged with surprising speed on payments and identity, but it has not seriously examined its deepest layer - settlement - and that is where the next argument in this industry will be fought. Our position, argued in Part IV with its assumptions openly stated: when autonomous counterparties transact at incredible speeds with no legal recourse between them, final settlement gravitates toward the most neutral, most attack-costly, longest-lived ledger that exists. Today that ledger is Bitcoin - which is why we hold that, in the limit, if it doesn't settle on Bitcoin, it doesn't settle at all.

Disclosure. GOAT Network builds Bitcoin-secured infrastructure for the agent economy - x402 payments, ERC-8004 identity, and a zkEVM environment that anchors to Bitcoin via a BitVM2/3-based bridge. We have an obvious commercial interest in the conclusion of Part IV. A truthful report names its bias and then earns its argument anyway: every adoption figure here is sourced, every caveat that cuts against us is printed, and the strongest counterarguments to our own thesis get their own section. Judge the case on the evidence.

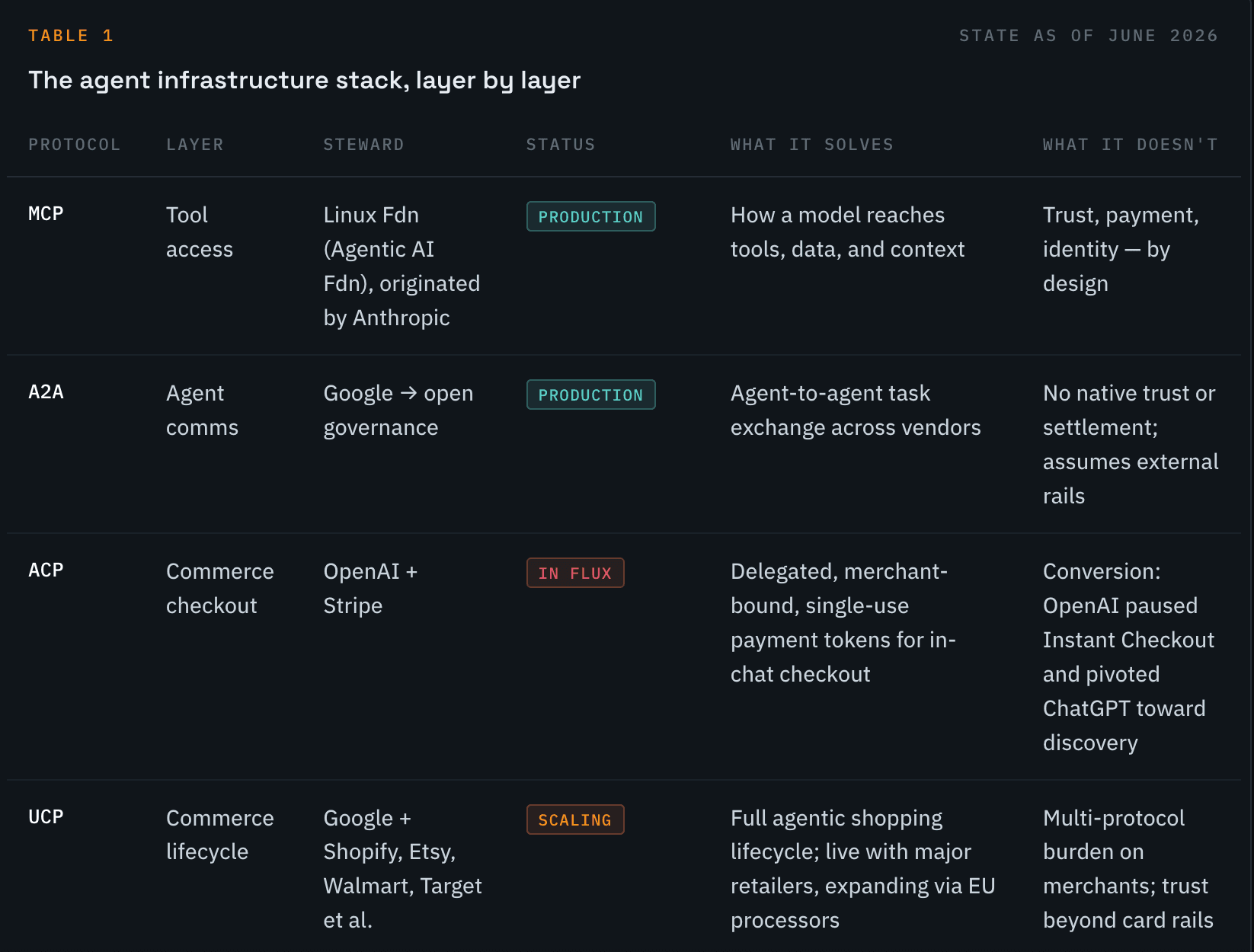

01/ The Inventory - What actually exists: the 2026 protocol stack

Eighteen months ago "agent infrastructure" meant a framework for chaining LLM calls. Today it means a layered protocol stack with named standards, foundation governance, and production deployments. The consolidation happened in roughly four waves: tool connectivity (MCP, late 2024–2025), agent-to-agent communication (A2A, 2025), commerce and mandates (ACP, UCP, AP2, late 2025), and onchain value - payments and identity (x402, ERC-8004, 2025–2026).

Two governance events mark the maturation. Anthropic donated the Model Context Protocol to the Linux Foundation's Agentic AI Foundation in December 2025, and Coinbase donated x402 to a Linux Foundation–hosted x402 Foundation in April 2026 - the standard move a protocol makes when it wants to outlive its creator. Visa, Stripe, Mastercard, Google, Cloudflare and Fireblocks have all attached themselves to one or more layers of this stack. The table below is the honest inventory.

Sources: Linux Foundation/Agentic AI Foundation announcements; x402 Foundation; OpenAI-Stripe ACP documentation; Google UCP/AP2 partner disclosures; ERC-8004 mainnet deployment records. Status labels are our editorial judgment.

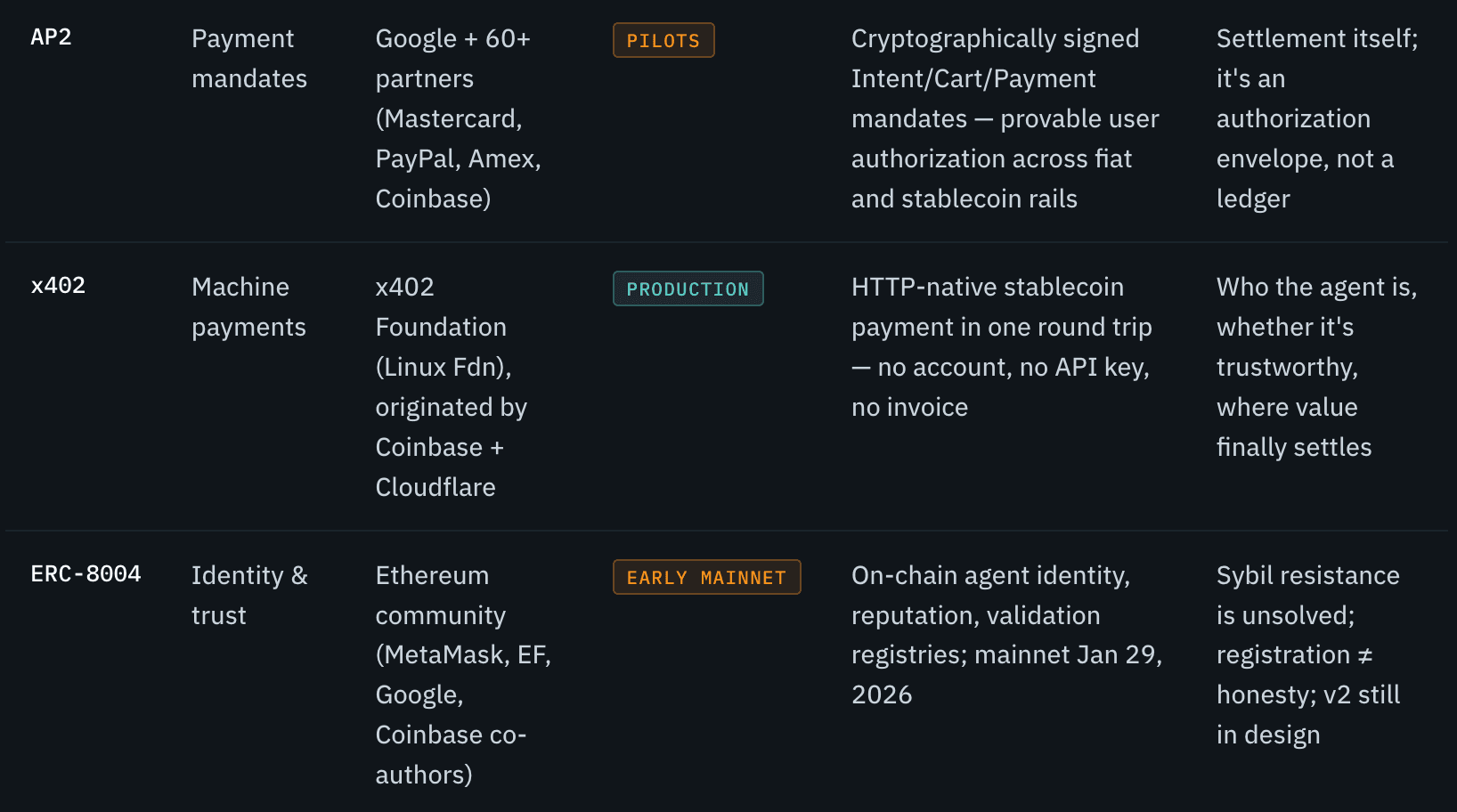

The payments layer found product-market fit first

The single most load-bearing dataset in agent infrastructure is x402's onchain history, because unlike framework download counts it cannot be faked cheaply and cannot be narrated around.

Chainalysis counts well over 100 million cumulative x402 transactions on Base alone through Q1 2026, from a near-zero start in mid-2025. Protocol-wide figures cited at the launch of Coinbase's Agent.market directory in April 2026 put cumulative activity around 165 million transactions, roughly $50 million in cumulative volume, and about 69,000 active agents. Stripe shipped x402 support in February 2026; Cloudflare wired it into pay-per-crawl, converting bot mitigation into a pricing mechanism; Visa attached it to its Trusted Agent Protocol; Fireblocks joined the foundation in May 2026 with enterprise spend-governance tooling.

Cumulative trajectory is approximate, interpolated between published checkpoints: Chainalysis (100M+ on Base through Q1 2026), Solana Foundation (35M on Solana by March 2026), and protocol-wide totals of ~165M transactions/~$50M volume cited at the April 2026 Agent.market launch. Shape, not month-precision, is the claim.

And the transactions are getting more serious

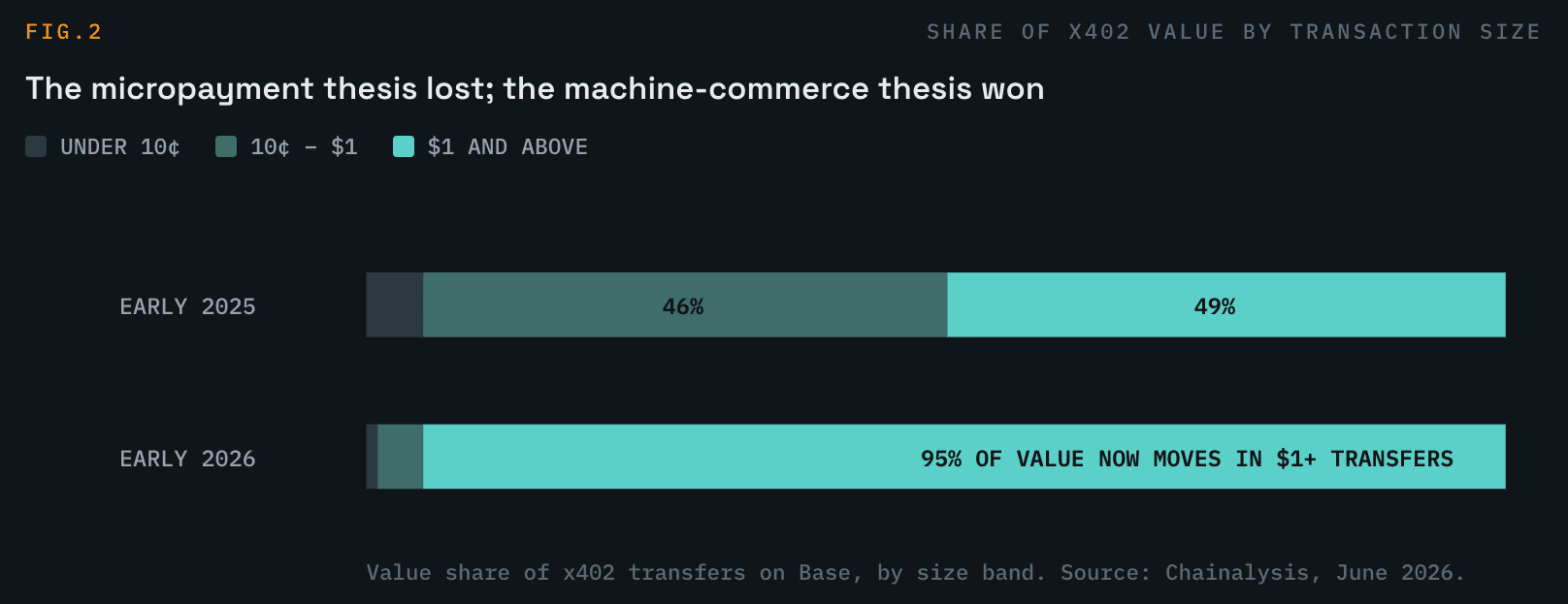

The more telling signal is not the count but the composition. Chainalysis finds that transfers of $1 or more carried about 49% of x402 value in early 2025-style activity and 95% by early 2026, while the 10¢–$1 band collapsed from 46% to 4%.

Sub-cent micropayment experimentation is giving way to funded wallets making purposeful purchases - data, inference, search, booking. Chainalysis also reports a roughly fourfold improvement in user retention over six months, and that x402 wallets hold more diverse tokens and larger balances than typical Base wallets. The protocol is acquiring customers, not just transactions.

The sub-$1 band didn't disappear in count - x402 still processes large numbers of tiny calls - but its economic weight collapsed. Agents fund wallets and buy real services.

Identity arrived second, and perhaps louder than it deserved

ERC-8004 - three lightweight registries for agent identity, reputation, and validation, co-authored by contributors from MetaMask, the Ethereum Foundation, Google, and Coinbase - went live on Ethereum mainnet on January 29, 2026. Adoption headlines came fast: more than 20,000 agent registrations across Ethereum, BNB Chain and Base within two weeks, and reports of over 160,000 registered agents by spring, with BNB Chain leading deployments. Production usage exists - one yield-optimization service reported eight figures of deposits managed by 8004-registered agents within weeks of launch.

Now the truthful part. Registration is nearly free on L2s, which means registration counts are the easiest metric in this stack to inflate. Onchain analysts have openly asked whether the deployment wave is organic or partially a way to simulate network activity on chains short of human users. Sybil resistance is an acknowledged open problem in the standard itself; an identity NFT proves continuity, not honesty.

We use ERC-8004 in production and believe in it - and we would caution anyone against reading 160,000 registrations as 160,000 economic actors. The retention-adjusted truth is likely one to two orders of magnitude smaller.

02/ The Correction - The honest read: a drawdown, a pause, and a denominator

An industry-leading report earns the adjective by printing the numbers that cut against the narrative. There are three.

1. The activity drawdown was real

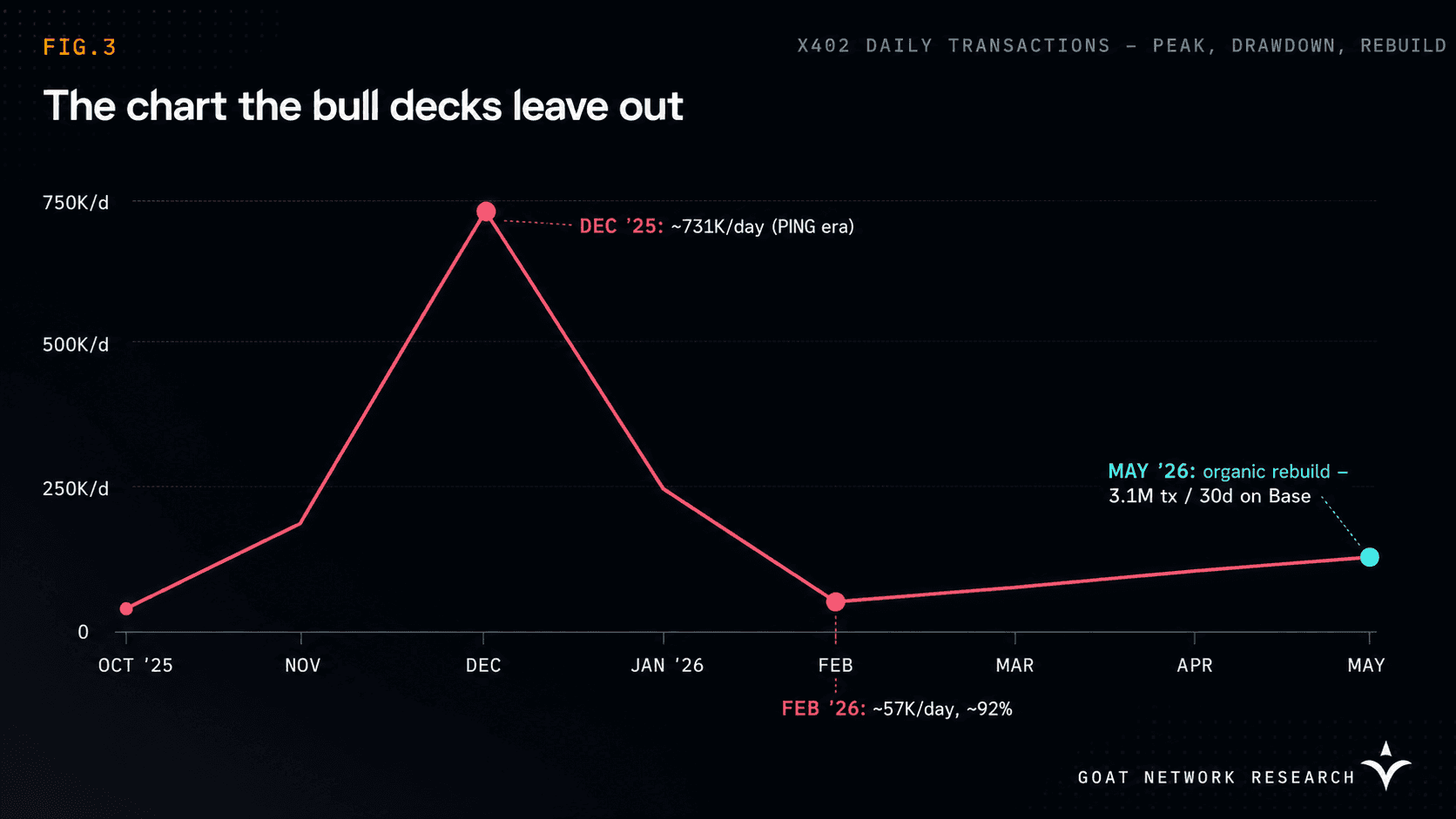

x402 daily transactions peaked near 731,000 in December 2025, inflated by the PING memecoin experiment and incentive-driven traffic, then fell over 90% to roughly 57,000 per day by February 2026. That is not a detail; it is the difference between a hockey stick and an S-curve with a speculative spike on it.

The constructive read - which the subsequent data supports - is that this was DeFi-summer-style normalization: by late May 2026, Base alone was back to 3.1 million x402 transactions per 30 days with $1.2M transferred, with sellers up 23% and buyers up 37% month over month, on visibly more organic usage. But anyone extrapolating from the December peak was extrapolating from a memecoin.

Daily figures interpolated between published checkpoints (731K/day December peak and 57K/day February trough per BlockEden; 3.1M per 30 days on Base as of May 29, 2026 per Base). Red marks the speculative cycle; cyan marks the organic baseline now compounding.

2. The human-commerce front stalled

Agentic checkout for humans - the consumer-facing wing of this story - hit friction in early 2026. OpenAI paused Instant Checkout in ChatGPT and repositioned around discovery and comparison. Walmart reported conversion roughly three times lower for in-chat purchases versus redirecting shoppers to its own site.

This is not to say that agentic commerce is fake; Google's UCP went live with Etsy and Wayfair and is expanding through European processors, Amazon widened "Buy for Me," and Gap is building on Gemini. But the lesson is that the near-term center of gravity is machine-to-machine - agents buying data, compute, inference, and API calls from other software - not chat windows replacing checkout pages. The onchain rails are where that M2M economy is measurable.

3. The denominator is brutal

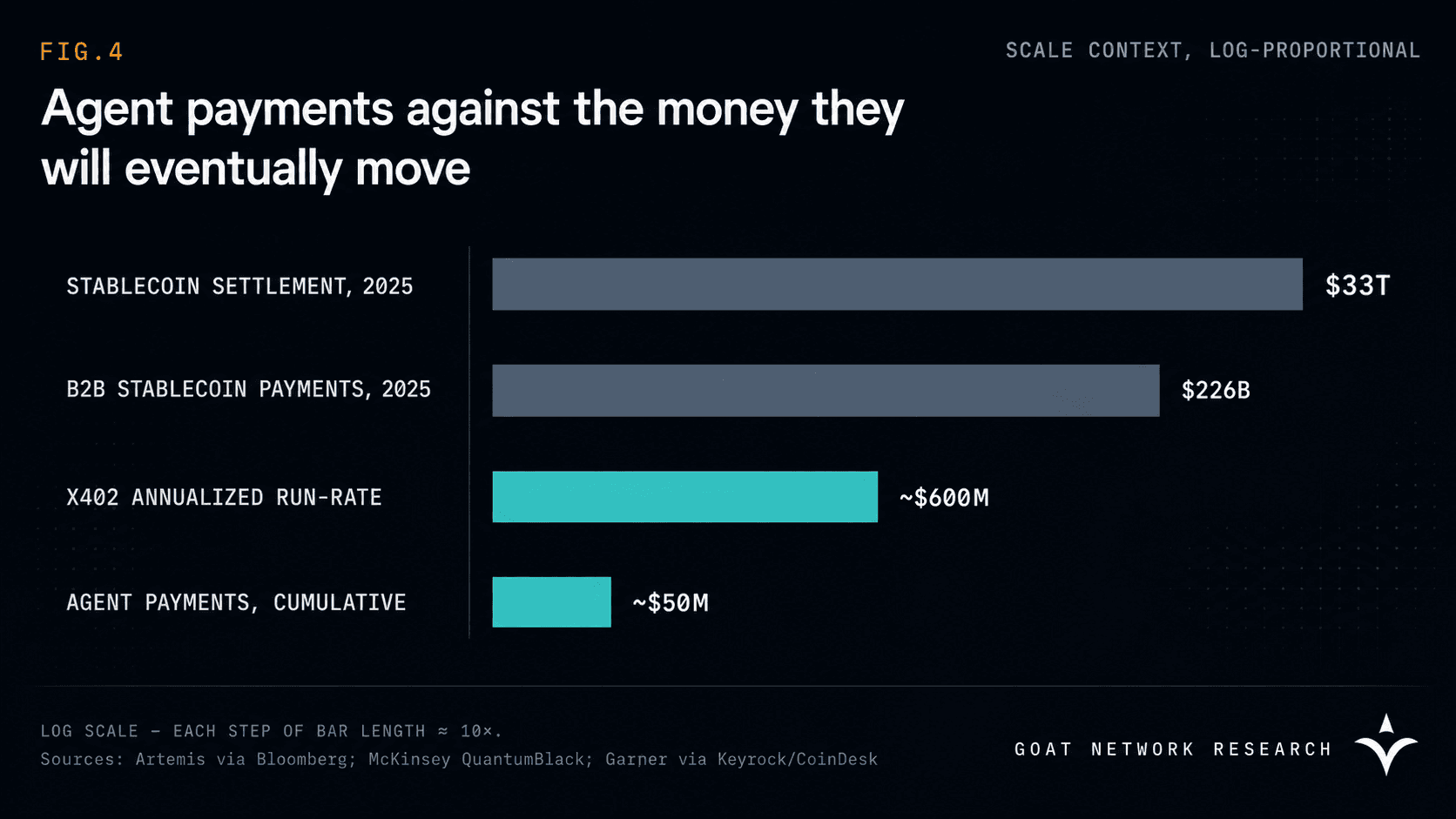

Stablecoins settled roughly $33 trillion in 2025 by Artemis's count (some methodologies put gross figures higher, ~$9 trillion after filtering automated flows). Against that, ~$50 million of cumulative agent-payment volume is approximately 0.0001%. One analysis tallied roughly 1.4 billion agent payments over nine months, 98.6% in USDC, averaging $0.31 each - real, but small. We consider this the single most clarifying statistic in the field: the rails work, the liquidity exists, and the agents have barely begun to spend. Whether you read that as "nothing is happening" or "everything is about to" is the entire bull/bear divide of 2026.

On a linear scale the bottom two bars would be invisible. That is the point: agent-native payment volume is six orders of magnitude below the settlement liquidity already waiting for it.

Method note. Forecast and volume figures in this field vary by methodology and are sometimes laundered through aggregator blogs. Where sources conflict (e.g. $33T vs $46T stablecoin volume), we cite the more conservative, better-attributed figure and flag the range. Treat every number above as decision-grade direction, not audit-grade precision.

03/ The Gaps - What the stack still doesn't have

Mapping the inventory against what a functioning machine economy requires exposes five gaps. Four are being worked on. The fifth is being assumed away.

Authorization and liability. AP2's signed mandates, ACP's merchant-bound tokens, and the card networks' Know-Your-Agent programs (Visa TAP, Mastercard Agent Pay, now extended to issuing banks through FIS) all attack the same question: how does anyone prove an agent acted within its principal's authority - and who eats the loss when it didn't? Progress is real; case law is nonexistent. Expect the first major agent-payment liability dispute to shape this layer more than any spec will.

Identity that means something. ERC-8004 gives agents persistent identity; World's AgentKit binds agents to proof of a unique human; reputation registries accumulate history. None of it yet solves the cold-start problem - why trust a new agent? - or the Sybil problem at an adversarial scale. Identity is shipped; trust is v2.

Discovery. Agent.market, GNS-style naming systems, UCP merchant profiles and ERC-8004 agent cards are early phone books. Fragmented, mutually incompatible, improving monthly.

Spend governance. Session keys, scoped wallets, per-counterparty limits, Fireblocks-grade policy engines. The enterprise tooling wave of 2026 - necessary, unglamorous, well underway.

Settlement. And then there is the layer everyone inherits and nobody chose. Nearly all agent value today settles as USDC on Base or Solana - which means its finality rests, in sequence, on a young L2's security council or a high-throughput chain's validator set, and on a regulated issuer with a freeze function and a redemption promise. For $50 million of cumulative experimentation, that is fine. The question of Part IV is whether it remains fine at the scale everyone in this industry is forecasting.

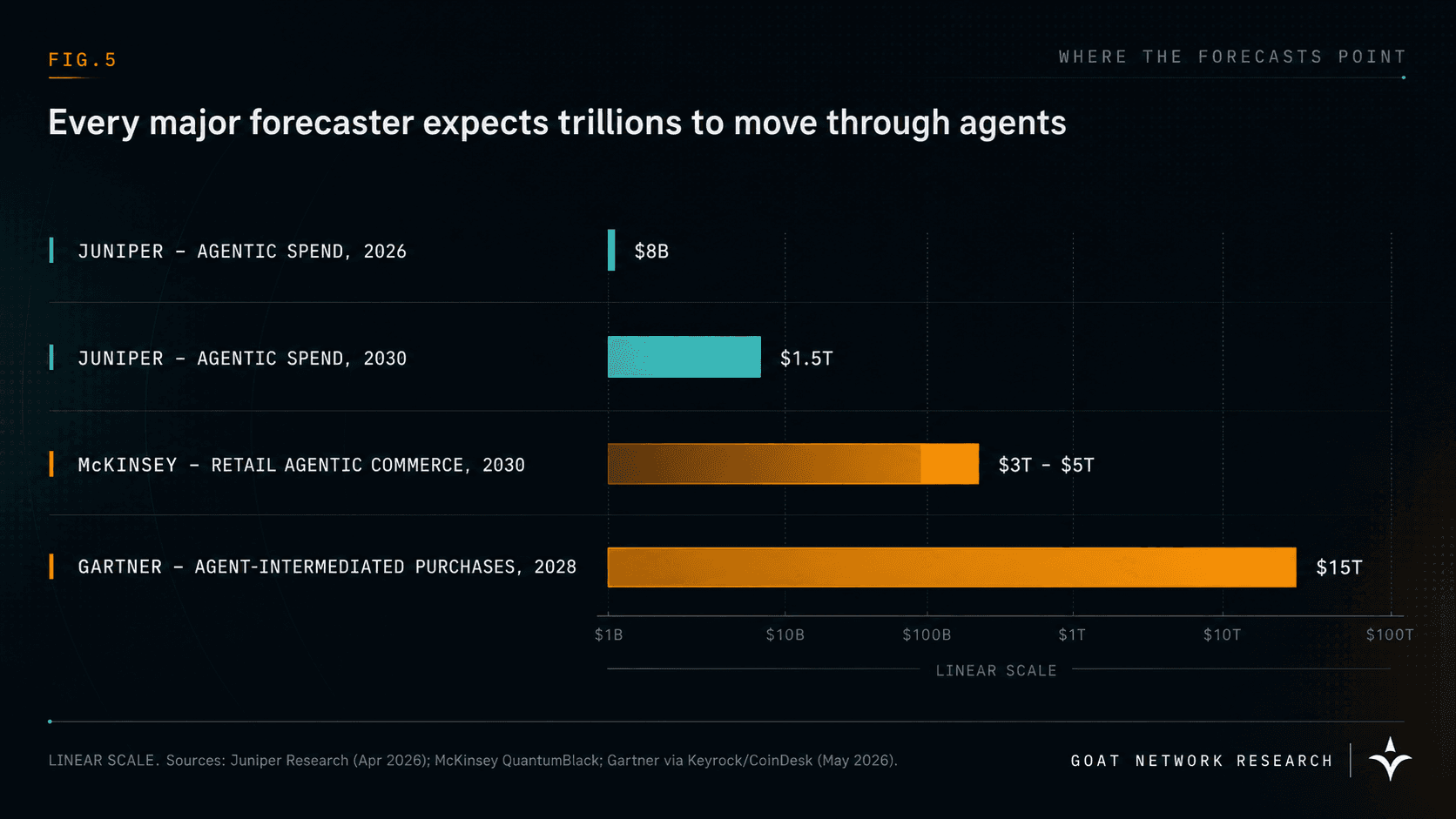

Forecasts measure different things - direct spend vs. influenced purchases - and all deserve skepticism. But note the spread: even the most conservative 2030 number is ~30,000× current cumulative agent-payment volume. Infrastructure decisions made now are decisions about that world, not this one.

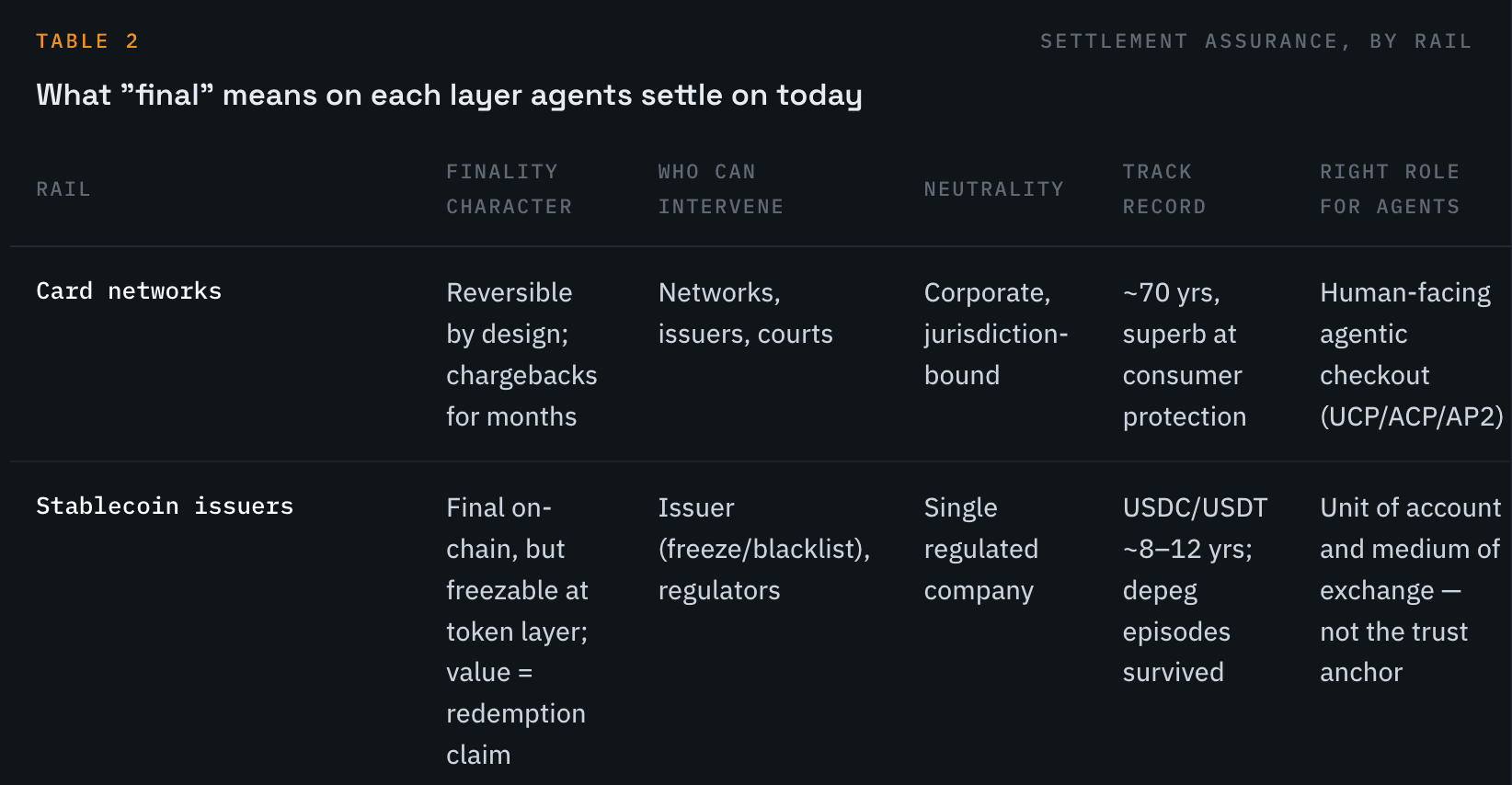

04/ The Settlement Question - Payment is a message. Settlement is a fact.

Here is the distinction the agent-infrastructure conversation keeps blurring, and which this entire report has been building toward.

A payment is a message: an instruction, an authorization, a balance update inside some system. A settlement is a fact: the point past which the transfer cannot be reversed, censored, or renegotiated by any party - including the operator of the system it happened on.

Card networks make payments in milliseconds and settle in days, with chargeback windows measured in months. Stablecoin transfers feel final in seconds, but their finality is layered: the chain can reorganize or its operators can intervene, and above the chain sits an issuer that can freeze addresses and stands behind a redemption promise. None of this is a criticism - reversibility is a feature for human commerce, where courts, contracts, and customer support absorb disputes.

Machine commerce breaks that assumption in three specific ways:

No recourse between counterparties. When an agent in one jurisdiction buys inference from an anonymous agent in another, there is no merchant agreement, no chargeback process, no small-claims court. The transaction's finality is the entire legal system available to it. The weaker the settlement guarantee, the more trust the agents must place in intermediaries — which is exactly the dependency this stack was built to remove.

Machine speed compounds counterparty exposure. An agent transacting thousands of times a day with hundreds of counterparties accumulates exposure to every layer beneath it: the sequencer, the validator set, the bridge, the issuer. Tail risks that are tolerable at human transaction frequency become actuarial certainties at machine frequency and decade horizons.

Neutrality becomes load-bearing. Agents will be operated from every jurisdiction on earth, including ones that sanction each other. A settlement layer with an identifiable operator, foundation, security council, or issuer is a settlement layer that can be pressured. The only rail that two mutually distrusting machine economies can both accept is one that neither - and no state - controls.

The agent economy is converging on open protocols for payments and identity while quietly assuming institutional guarantees for settlement. That assumption is the largest unpriced risk in the stack.

Comparing the settlement candidates honestly:

"Who can intervene" describes the cheapest realistic intervention path, not a prediction. Hashrate context: Bitcoin's network crossed 1 zettahash/s in January 2026; difficulty entered 2026 near all-time highs (~148T). Even the year's sharpest shock - a 30-40% hashrate drop during Winter Storm Fern - produced zero loss of finality.

The thesis, stated with its assumptions

Our position: if it doesn't settle on Bitcoin, it doesn't settle at all. Properly unpacked, that sentence is a claim about what the word "settle" can truthfully mean for autonomous counterparties. Everything short of the most neutral, most attack-costly ledger is deferred settlement - an IOU on some institution's continued solvency, cooperation, and political insulation. For humans, deferred settlement backed by law is usually optimal. For machines with no access to law, it is a stack of silent trust assumptions compounding at machine speed.

The argument holds if - and only if - four premises hold. We state them so they can be attacked:

P1 - Agent commerce becomes large and adversarial. If agents stay a $50M curiosity inside friendly jurisdictions, institutional settlement is fine and this thesis is irrelevant. Every forecast in Figure 5 — and the protocol investment by Visa, Stripe, Google and the Linux Foundation - bets against that.

P2 - Settlement assurance is priced eventually. Markets ignored counterparty risk in 2007 and in centralized crypto until 2022, then repriced it violently. We assume agent markets will reprice settlement risk after the first major freeze, reorg, or council intervention touching agent funds - not before.

P3 - Neutrality cannot be replicated by decree. Proof-of-work's security is purchased with physical energy outside the system; its neutrality emerged from 17 years without a controlling party. A consortium can copy the software; it cannot copy the history or the absence of an owner.

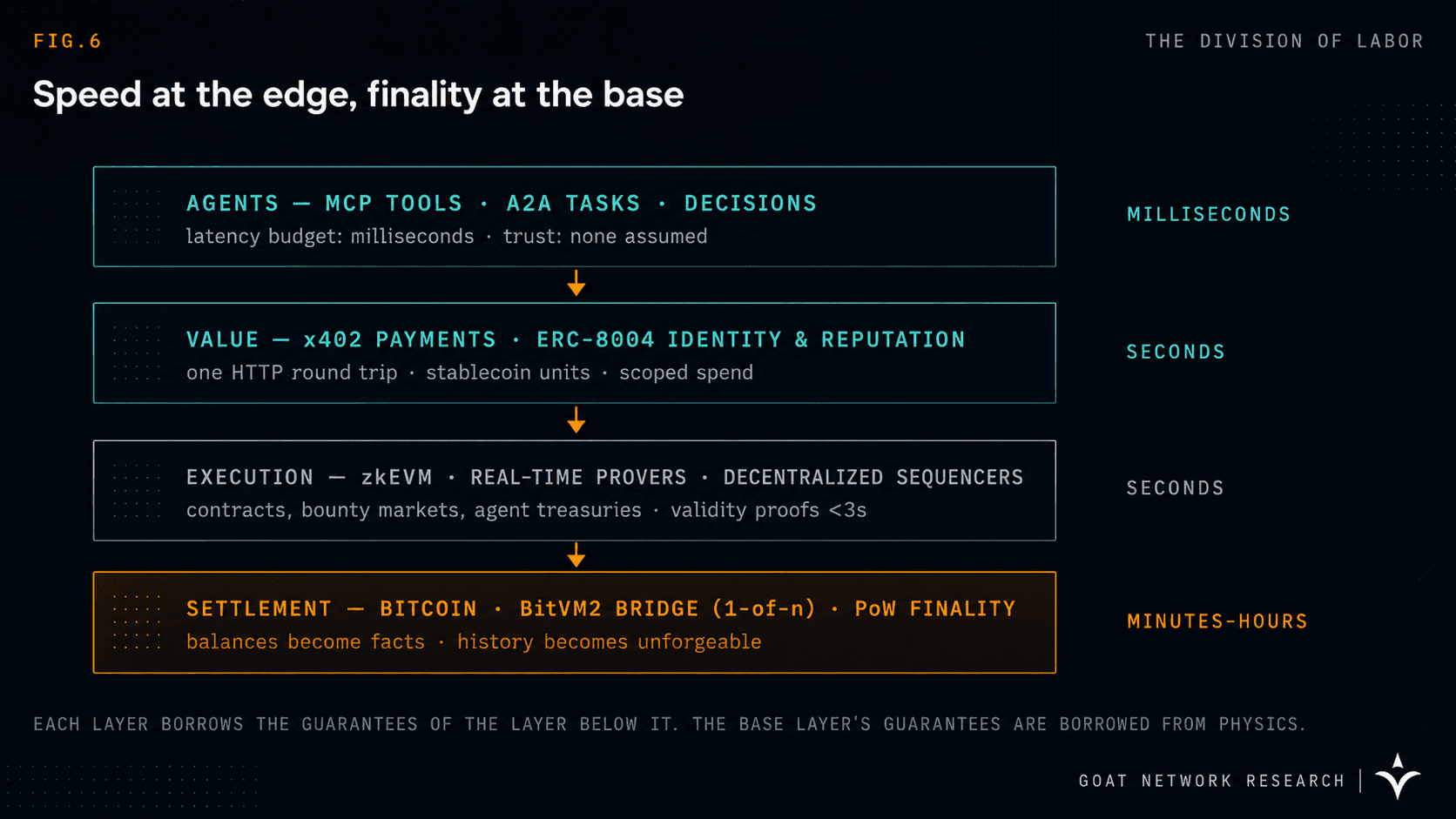

P4 - Bitcoin's programmability gap is closing without compromising the base layer. This was the weakest premise for a decade and is the one that changed. BitVM2/3-class bridges reduce trust in moving value to and from Bitcoin to a 1-of-n honesty assumption - any single honest participant can stop fraud - and real-time ZK proving (sub-3-second proofs are now in production testing, including in our own Ziren zkVM) makes it practical to verify arbitrary execution against Bitcoin. Settlement on Bitcoin no longer means computing on Bitcoin.

If you reject any premise, you should reject the conclusion - and you'll find our best arguments against ourselves below. But notice what the conclusion does not claim. It does not claim agents will transact on Bitcoin's base layer; seven transactions per second cannot host a machine economy and was never supposed to. It does not claim stablecoins lose; agents demonstrably prefer dollar units, and 98.6% of measured agent payments use USDC.

It claims something narrower and harder: that the bottom of the stack - the layer where balances become facts and reputations become history - gravitates to the ledger with the strongest finality, the longest record, and no owner. Payments at the speed of HTTP; settlement at the depth of proof-of-work.

The architecture GOAT Network ships today: x402 as native payment rail, ERC-8004 as native identity, a Type-1 zkEVM with real-time proving for execution, decentralized sequencers, and a BitVM2/3-based bridge anchoring to Bitcoin.

Steelmanning the other side

An objective report argues against itself. Four counterarguments deserve full weight:

"Ethereum already is the agent trust layer." True today, and not trivially. ERC-8004 lives there; the deepest smart-contract security culture lives there; economic finality via slashable stake is a coherent, battle-considered design. If you believe staked-capital finality is equivalent to expended-energy finality at decade horizons, the marginal value of Bitcoin anchoring shrinks substantially. Our response is that the two models fail differently - stake can be regulated, concentrated, and socially coordinated in ways amortized physical energy cannot - but we acknowledge this is the strongest rival position, and a plural settlement world is a live possibility.

"Agents settle in dollars, and dollars mean issuers." Correct, and it bounds our claim: anchoring a USDC balance to Bitcoin does not remove Circle from the picture. Bitcoin settlement is fully self-contained only for BTC-denominated value. Our expectation - a thesis, not a fact - is that as agent treasuries grow, a meaningful share of machine wealth holds the settlement asset itself precisely to shed issuer risk, the way nations hold gold. The early BTC-yield demand from institutions on our own network is consistent with this, and is also obviously the data we would notice first.

"Bitcoin's own security budget is a question." The honest caveat from our own side. As block subsidies halve, base-layer security increasingly depends on fee demand; analysts legitimately ask whether fees alone sustain a zettahash. We'd note the counter-dynamic: settlement-layer use - L2 anchoring, BitVM2 dispute games, institutional batching - is precisely the high-value, fee-insensitive demand that answers the question. The thesis is, in part, self-funding: if final settlement migrates to Bitcoin, the security budget problem dissolves; if it doesn't, the problem is real. We are building as if the first branch is true and watching the fee market like everyone else.

"BitVM2/3 and friends are young." Also true. The 1-of-n bridge assumption is the best trust model Bitcoin interoperability has ever had, and it is years old, not decades. Anyone who tells you Bitcoin L2 bridges are as proven as Bitcoin itself is selling something. They are, however, the only construction on the table whose trust assumptions reduce to Bitcoin plus one honest watcher - which is why we bet the company on maturing them rather than on multisig federations.

05/ Where This Goes - The truthful summary

The current state of agent infrastructure, compressed: coordination is solved (MCP, A2A - production, foundation-governed). Payments are solved and finding real demand (x402 - 165M transactions, growing transaction sizes, post-speculation organic compounding). Commerce is live but humbled (UCP scaling, ACP recalibrating, conversion data forcing realism). Identity is shipped but not yet trustworthy (ERC-8004 - mainnet, inflated counts, Sybil problem open). Authorization is being built by the incumbents (AP2, TAP, Agent Pay, KYA). And settlement is the layer nobody chose - inherited from whatever chain the payment rail happened to launch on, carrying institutional guarantees into a machine economy that exists precisely because it doesn't want them.

The numbers say the agent economy is six orders of magnitude smaller than its destination. That gap is the opportunity and the warning: everything structural is still up for grabs, and the defaults being set right now - in specs, in foundations, in which chain an SDK points at - will harden into the architecture trillions of dollars flow through. The industry has been commendably rigorous about how machines pay and who machines are. It has been incurious about where machine value finally rests.

We've made our argument and shown its assumptions. Value should move like information - instant, borderless, open to anything. Rules should execute as code. And trust, when the counterparties are machines with no court to appeal to, should settle on the one ledger that has never needed anyone's permission to keep its promises. Payments at the speed of HTTP. Settlement at the depth of proof-of-work.

If it doesn't settle on Bitcoin, it doesn't settle at all.

Sources & data notes

All figures paraphrased from the publications below; charts are original renderings of published checkpoints with interpolation noted in captions. Conflicting figures are flagged in the text.

[01] Chainalysis - "Inside x402: 100M Agentic Payments on Base" (June 2026): cumulative Base transactions, value-share by size band, retention and wallet-composition findings.

[02] Coinbase Agent.market launch coverage & x402 Foundation (Linux Foundation, April 2026): ~165M protocol-wide transactions, ~$50M cumulative volume, ~69K active agents; Stripe Machine Payments (Feb 2026); Visa TAP and Cloudflare pay-per-crawl integrations.

[03] BlockEden Research (March 2026): Solana x402 share (~49%, Feb 2026), 35M Solana transactions, ~$600M annualized run-rate, December 2025 peak (731K/day) and February 2026 trough (57K/day).

[04] Base network update (May 29, 2026): 3.1M x402 transactions and $1.2M transferred per trailing 30 days; seller/buyer growth rates.

[05] ERC-8004 deployment records and coverage (Jan–Apr 2026): mainnet launch Jan 29, 2026; 20K+ registrations in two weeks; ~160K reported registrations by spring with BNB Chain leading; organic-vs-synthetic deployment questions raised by on-chain analysts.

[06] Google AP2 announcement (Sept 2025) and partner disclosures; Forrester agentic-payments timeline (2026): FIS/Visa/Mastercard KYA programs, UCP capability expansion, Gap/Gemini.

[07] commercetools Agentic Commerce Radar (2026): OpenAI Instant Checkout pause; Walmart in-chat conversion findings.

[08] Artemis via Bloomberg: $33T stablecoin settlement volume in 2025 (+72% YoY); McKinsey: B2B stablecoin payments $226B (+733%); alternative gross figures up to ~$46T / ~$9T adjusted noted as methodology-dependent.

[09] Keyrock report via CoinDesk (May 2026): Gartner $15T agent-intermediated purchases by 2028; McKinsey $3–5T retail agentic commerce by 2030; Juniper Research (Apr 2026): $8B (2026) → $1.5T (2030).

[10] Industry payment analysis (2026): ~1.4B agent payments over nine months, 98.6% USDC, ~$0.31 average - directional, methodology not independently verified.

[11] Bitcoin network data (Jan–Feb 2026): hashrate crossing 1 ZH/s; difficulty ~148T entering 2026; Winter Storm Fern drawdown and recovery with no loss of finality.

[12] GOAT Network technical documentation: BitVM2 bridge (1-of-n assumption), Ziren zkVM real-time proving (<3s), decentralized sequencer network, native x402 + ERC-8004 + AgentKit stack.

Published for discussion; not financial advice.