2025-11-19

This crypto-asset white paper has not been approved by any competent authority in any Member State of the European Union. The person seeking admission to trading of the crypto-asset is solely responsible for the content of this crypto-asset white paper.

This crypto-asset white paper complies with Title II of Regulation (EU) 2023/1114 of the European Parliament and of the Council and, to the best of the knowledge of the management body, the information presented in the crypto-asset white paper is fair, clear and not misleading and the crypto-asset white paper makes no omission likely to affect its import.

The crypto-asset referred to in this crypto-asset white paper may lose its value in part or in full, may not always be transferable and may not be liquid.

Since the token has multiple functions (hybrid token), these are already conceptually not utility tokens within the meaning of the MiCAR within the definition of Article 3, 1. (9), due to the necessity “exclusively” being intended to provide access to a good or a service supplied by its issuer only.

The crypto-asset referred to in this white paper is not covered by the investor compensation schemes under Directive 97/9/EC of the European Parliament and of the Council or the deposit guarantee schemes under Directive 2014/49/EU of the European Parliament and of the Council.

Warning: This summary should be read as an introduction to the crypto-asset white paper. The prospective holder should base any decision to purchase this crypto–asset on the content of the crypto-asset white paper as a whole and not on the summary alone. The offer to the public of this crypto-asset does not constitute an offer or solicitation to purchase financial instruments and any such offer or solicitation can be made only by means of a prospectus or other offer documents pursuant to the applicable national law. This crypto-asset white paper does not constitute a prospectus as referred to in Regulation (EU) 2017/1129 of the European Parliament and of the Council or any other offer document pursuant to union or national law.

The GOATED tokens referred to in this white paper are crypto-assets other than EMTs and ARTs, and are issued on the GOAT network (2025-09-11 and according to DTI FFG shown in F.14). with a total number of 1,000,000,000 tokens.

Not applicable.

This white paper concerns the admission to trading of the crypto-asset "GOATED" by "GOAT Foundation" in accordance to Article 5 of REGULATION (EU) 2023/1114 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 31 May 2023 on markets in cryptoassets, and amending Regulations (EU) No 1093/2010 and (EU) No 1095/2010 and Directives 2013/36/EU and (EU) 2019/1937.

The following platforms are in scope for this while drafting up this white paper: Payward Global Solutions Limited. Further platforms are also being sought for this purpose in the future.

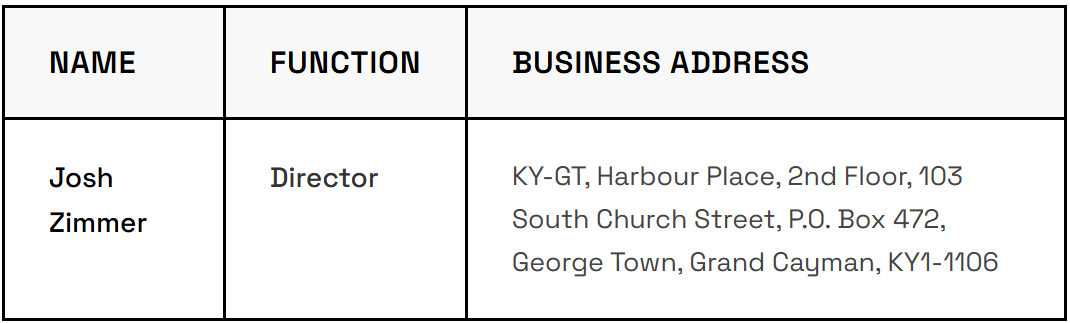

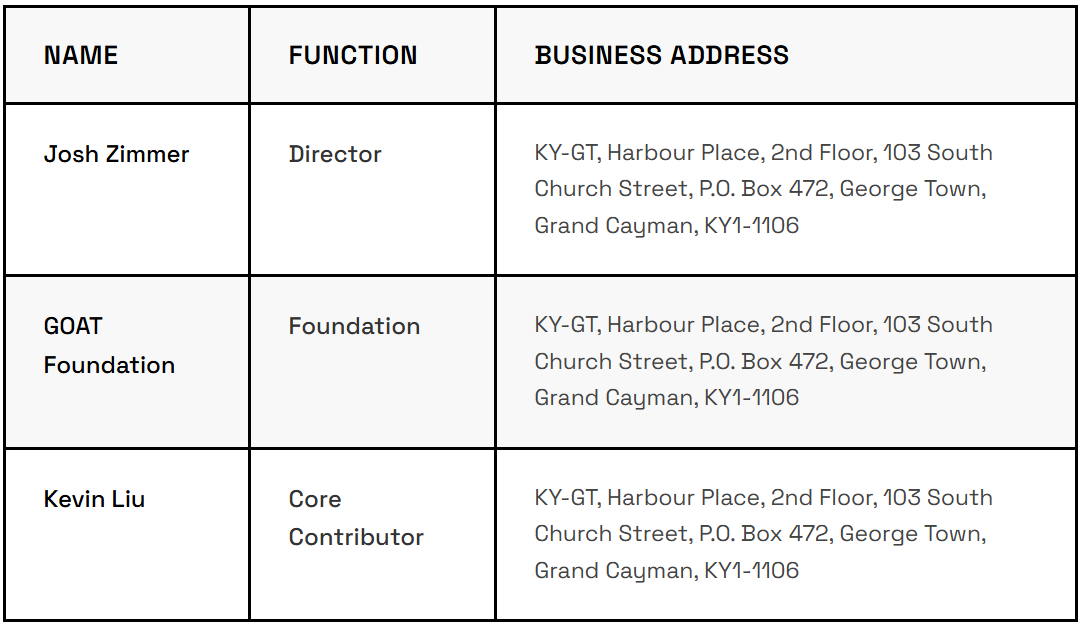

A.1 Name

GOAT Foundation

A.2 Legal form

4XP8

A.3 Registered address

KY-GT, Harbour Place, 2nd Floor, 103 South Church Street, P.O. Box 472, George Town, Grand Cayman, KY1-1106, Cayman Islands

A.4 Head office

Not applicable.

A.5 Registration date

2025-01-03

A.6 Legal entity identifier

Not available.

A.7 Another identifier required pursuant to applicable national law

IC-417101

A.8 Contact telephone number

Not available.

A.9 E-mail address

A.10 Response time (Days)

030

A.11 Parent company

Not applicable

A.12 Members of the management body

A.13 Business activity

The company was founded with the purpose of acting as a central foundation to support and drive the holistic development of the crypto project. Its primary mission is to enable, coordinate, and oversee the various initiatives that contribute to the growth and sustainability of the ecosystem. By providing strategic guidance, fostering collaboration among stakeholders, and ensuring alignment with the project’s long-term vision, the company serves as a stabilizing and empowering entity within the ecosystem. Over time, its level of involvement and influence may evolve in response to the project’s maturity, community participation, and changing market dynamics, ensuring that its role remains adaptive, transparent, and value-driven.

A.14 Parent company business activity

Not applicable.

A.15 Newly established

Yes

A.16 Financial condition for the past three years

Not applicable.

A.17 Financial condition since registration

The company was established in 2025. The preparation and adoption of financial statements will occur at and after the end of the fiscal year, which is the relevant accounting and preparation period under Cayman Islands law. As of this submission, no complete fiscal year has concluded, and therefore no completed and adopted financial statements exist. In addition, as an ownerless foundation company limited by guarantee, the company does not and will never have a capitalization table displaying shareholders/owners.

As of the date of this white paper, the company’s assets consist of control of 15% of the treasury of GOATED, the fair market value of which fluctuates. The company has approximately $100,000 in liabilities.

B.1 Issuer different from offeror or person seeking admission to trading

Yes

B.2 Name

The GOAT Foundation plays an important role in supporting the ongoing development of the ecosystem and contributes to its long-term advancement. However, because the crypto-assets are issued from the network, the GOAT Foundation does not hold a formally defined role as the issuer of the crypto-asset. The crypto-asset is therefore to be regarded as decentralized, without a designated issuer formally involved in its issuance.

B.3 Legal form

Not applicable.

B.4. Registered address

Not applicable.

B.5 Head office

Not applicable.

B.6 Registration date

Not applicable.

B.7 Legal entity identifier

Not applicable.

B.8 Another identifier required pursuant to applicable national law

Not applicable.

B.9 Parent company

Not applicable.

B.10 Members of the management body

Not applicable.

B.11 Business activity

Not applicable.

B.12 Parent company business activity

Not applicable.

C.1 Name

Not applicable.

C.2 Legal form

Not applicable.

C.3 Registered address

Not applicable.

C.4 Head office

Not applicable.

C.5 Registration date

Not applicable.

C.6 Legal entity identifier

Not applicable.

C.7 Another identifier required pursuant to applicable national law

Not applicable.

C.8 Parent company

Not applicable.

C.9 Reason for crypto-Asset white paper Preparation

Not applicable.

C.10 Members of the Management body

Not applicable.

C.11 Operator business activity

Not applicable.

C.12 Parent company business activity

Not applicable.

C.13 Other persons drawing up the crypto-asset white paper according to Article 6(1), second subparagraph, of Regulation (EU) 2023/1114

Crypto Risk Metrics GmbH, Lange Reihe 73, 20099 Hamburg

C.14 Reason for drawing the white paper by persons referred to in Article 6(1), second subparagraph, of Regulation (EU) 2023/1114

Crypto Risk Metrics GmbH, Lange Reihe 73, 20099 Hamburg, was mandated to support the process of drawing up the white paper by the person mentioned in Part A.

D.1 Crypto-asset project name

Long Name: GOAT Network Token, Short Name: GOATED according to the Digital Token Identifier Foundation (www.dtif.org, DTI see F.13, FFG DTI see F.14 as of 2025-08-25).

D.2 Crypto-assets name

Long Name: GOAT Network Token

D.3 Abbreviation

Short Name: GOATED

D.4 Crypto-asset project description

The project is designed to extend the functionality of Bitcoin by enabling decentralized applications and yield-generating mechanisms anchored to Bitcoin security in the future. The network operates as a Proof-of-Stake chain, where sequencer nodes participate in consensus through a combination of staked wrapped BTC and the token GOATED. While wrapped BTC serves as the gas token for transaction fees, the GOATED token functions as the consensus token required for staking and block production. In addition, the network supports bridged assets from external ecosystems, which are intended to increase liquidity and transactional activity within the network.

D.5 Details of all natural or legal persons involved in the implementation of the crypto-asset

D.6 Utility Token Classification

The token does not classify as a utility token.

D.7 Key Features of Goods/Services for Utility Token Projects

Not applicable.

D.8 Plans for the token

The development of the project has so far been marked by milestones primarily related to the technical implementation of the underlying network. These include, for example, the launch of the chain itself and the progressive implementation of functionalities that aim to enable anchoring to the Bitcoin mainnet. Publicly communicated milestones have therefore largely focused on the advancement of the overall ecosystem rather than the token itself.

Looking ahead, further milestones are expected to be linked to the expansion of network functionality, interoperability, and ecosystem growth. However, these developments are directed at the infrastructure level, and the concrete implications for the GOATED token cannot be precisely defined at this stage. Future outcomes depend on broader technological and market developments and cannot be predicted with certainty.

Consequently, no assurances or guarantees can be given regarding the realization of such future developments.

D.9 Resource allocation

The allocation of GOATED tokens is divided across several categories. Approximately 15.58% is reserved for investors, 7% for airdrop distributions, 15% for the treasury, 20% for the team and early contributors, 3% for advisors and key partners, and 39.42% for the mining pool reserve.

As a result, the effective circulating supply of the token will not correspond to the full allocation immediately, but will change over time depending on how vesting schedules and release mechanisms introduce tokens into the market. These mechanisms can influence token availability and thereby impact market dynamics.

The investor must be aware that a public address cannot necessarily be assigned to a single person or entity, which limits the ability to determine exact economic influence or future actions. Token distribution changes can negatively impact the investor.

D.10 Planned use of Collected funds or crypto-Assets

Not applicable, as this white paper was drawn up for the admission to trading and not for collecting funds for the crypto-asset-project.

E.1 Public offering or admission to trading

The white paper concerns the admission to trading (i. e. ATTR).

E.2 Reasons for public offer or admission to trading

The crypto asset is to be listed on the platforms: Payward Global Solutions Limited. Additional platforms are not excluded in the future.

E.3 Fundraising target

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.4 Minimum subscription goals

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.5 Maximum subscription goals

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.6 Oversubscription acceptance

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.7 Oversubscription allocation

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.8 Issue price

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.9 Official currency or any other crypto-assets determining the issue price

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.10 Subscription fee

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.11 Offer price determination method

Once the token is admitted to trading its price will be determined by demand (buyers) and supply (sellers).

E.12 Total number of offered/traded crypto-assets

The total supply of the crypto-asset is set at 1,000,000,000 units.

E.13 Targeted holders

ALL

E.14 Holder restrictions

The Holder restrictions are subject to the rules applicable to the Crypto Asset Service Provider as well as additional restrictions the Crypto Asset Service Providers might set in force.

E.15 Reimbursement notice

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.16 Refund mechanism

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.17 Refund timeline

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.18 Offer phases

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.19 Early purchase discount

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.20 Time-limited offer

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.21 Subscription period beginning

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.22 Subscription period end

ANot applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.LL

E.23 Safeguarding arrangements for offered funds/crypto- Assets

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.24 Payment methods for crypto-asset purchase

The payment methods are subject to the respective capabilities of the Crypto Asset Service Provider listing the crypto-asset.

E.25 Value transfer methods for reimbursement

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.26 Right of withdrawal

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.27 Transfer of purchased crypto-assets

The transfer of purchased crypto-assets are subject to the respective capabilities of the Crypto Asset Service Provider listing the crypto-asset.

E.28 Transfer time schedule

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

E.29 Purchaser's technical requirements

The technical requirements that the purchaser is required to fulfil to hold the cryptoassets of purchased crypto-assets are subject to the respective capabilities of the Crypto Asset Service Provider listing the crypto-asset.

E.30 Crypto-asset service provider (CASP) name

Not applicable.

E.31 CASP identifier

Not applicable.

E.32 Placement form

Not applicable.

E.33 Trading platforms name

Payward Global Solutions Limited. Other platforms are also planned for future listing.

E.34 Trading platforms Market identifier code (MIC)

Payward Global Solutions Limited: PGSL.

Other platforms are also planned for future listing.

E.35 Trading platforms access

This depends on the trading platform listing the asset.

E.36 Involved costs

This depends on the trading platform listing the asset. Investors should always review the current fee structures of platforms before making trading decisions. Furthermore, costs may occur for making transfers out of the platform (i. e. "gas costs" for blockchain network use that may exceed the value of the crypto-asset itself).

E.37 Offer expenses

Not applicable, as this crypto-asset white paper concerns the admission to trading and not the offer of the token to the public.

E.38 Conflicts of interest

Payward Global Solutions Limited, as a MiCAR-compliant Crypto Asset Service Provider, maintains a conflict of interest policy governing conflicts of interests arising in relation to its business. This conflict of interest policy governs, among other things, the interactions between the crypto asset service provider and the individuals disclosed in D.5 who are involved in the implementation of the GOATED token.

GOAT Foundation maintains a separate conflicts of interest policy. It also maintains separate written agreements prohibiting the unlawful use of confidential information by recipients.

Due to the fact that this white paper is intended for all MiCAR-compliant Crypto Asset Service Providers, potential investors should always check the conflicts of interest policy of their respective counterparty.

E.39 Applicable law

Not applicable, as it is referred to on "offer to the public" and in this white-paper, the admission to trading is sought.

E.40 Competent court

Not applicable, as it is referred to on "offer to the public" and in this white-paper, the admission to trading is sought.

F.1 Crypto-asset type

The crypto-asset described in the white paper is classified as a crypto-asset under the Markets in Crypto-Assets Regulation (MiCAR) but does not qualify as an electronic money token (EMT) or an asset-referenced token (ART). It is a digital representation of value that can be stored and transferred using distributed ledger technology (DLT) or similar technology, without embodying or conferring any rights to its holder.

The asset does not aim to maintain a stable value by referencing an official currency, a basket of assets, or any other underlying rights. Instead, its valuation is entirely marketdriven, based on supply and demand dynamics, and not supported by a stabilization mechanism. It is neither pegged to any fiat currency nor backed by any external assets, distinguishing it clearly from EMTs and ARTs.

Furthermore, the crypto-asset is not categorized as a financial instrument, deposit, insurance product, pension product, or any other regulated financial product under EU law. It does not grant financial rights, voting rights, or any contractual claims to its holders, ensuring that it remains outside the scope of regulatory frameworks applicable to traditional financial instruments.

F.2 Crypto-asset functionality

Not The GOATED token primarily serves as the consensus token of the network. Sequencer nodes are required to stake GOATED, alongside wrapped BTC, in order to participate in block production and validation under the Proof-of-Stake mechanism. This staking function is intended to align incentives and support the security of the network., as this crypto-asset white paper concerns the admission to trading and not the offer of the token to the public.

The token does not operate as the gas token for transactions, as fees within the network are paid in wrapped BTC bridged from the Bitcoin mainnet. GOATED is therefore not directly required for ordinary user transactions but is linked to the functioning of the consensus layer.

In addition, the network supports bridged assets from external blockchains, which may be used for liquidity provision and transactions. While these activities contribute to the ecosystem as a whole, the direct role of GOATED remains limited to its consensus and staking function.

F.3 Planned application of functionalities

Looking ahead, further milestones are expected to be linked to the expansion of network functionality, interoperability, and ecosystem growth. However, these developments are directed at the infrastructure level, and the concrete implications for the GOATED token cannot be precisely defined at this stage. Future outcomes depend on broader technological and market developments and cannot be predicted with certainty.

Consequently, no assurances or guarantees can be given regarding the realization of such future developments.

F.4 Type of crypto-asset white paper

The white paper type is "other crypto-assets" (i. e. "OTHR").

F.5 The type of submission

The white paper submission type is "MODI", which stands for a modified white paper.

F.6 Crypto-asset characteristics

The tokens are crypto-assets other than EMTs and ARTs, which are available on the Goat network. The tokens are fungible (up to 18 digits after the decimal point). The tokens are a digital representation of value, and have no inherent rights attached as well as no intrinsic utility.

F.7 Commercial name or trading name

GOAT Network

F.8 Website of the issuer

Since there is no formal issuer of the token, this is not applicable. Further information regarding the protocol, the broader ecosystem, and the Token is available at: https://www.goat.network/.

F.9 Starting date of offer to the public or admission to trading

2025-12-17

F.10 Publication date

2025-12-17

F.11 Any other services provided by the issuer

It is not possible to exclude a possibility that the issuer of the token provides or will provide other services not covered by Regulation (EU) 2023/1114 (i.e. MiCAR).

F.12 Language or languages of the crypto-asset white paper

EN

F.13 Digital token identifier code used to uniquely identify the crypto-asset or each of the several crypto assets to which the white paper relates, where available

3H75459K2

F.14 Functionally fungible group digital token identifier, where availableercial name or trading name

S1NP9MHTB

F.15 Voluntary data flag

Mandatory.

F.16 Personal data flag

The white paper does contain personal data.

F.17 LEI eligibility

The issuer should be eligible for a Legal Entity Identifier.

F.18 Home Member State

Ireland

F.19 Host Member States

Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Italy, Latvia, Lithuania, Luxembourg, Malta, Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden

G.1 Purchaser rights and obligations

The crypto-asset does not grant any legally enforceable or contractual rights or obligations to its holders or purchasers.

Any functionalities accessible through the underlying technology are of a purely technical or operational nature and do not constitute rights comparable to ownership, profit participation, governance, or similar entitlements known from traditional financial instruments.

Accordingly, holders do not acquire any claim capable of legal enforcement against the issuer or any third party.

G.2 Exercise of rights and obligations

As the crypto-asset does not establish any legally enforceable rights or obligations, there are no applicable procedures or conditions for their exercise.

Any interaction or functionality that may be available within the technical infrastructure of the project - such as participation mechanisms or protocol-level features - serves an operational purpose only and does not create or evidence a contractual or statutory entitlement.

G.3 Conditions for modifications of rights and obligations

Because the crypto-asset does not confer legally enforceable rights or obligations, there are no conditions or mechanisms under which such rights could be modified.

Adjustments to the technical protocol, smart contract logic, or related systems may occur in the ordinary course of development or maintenance.

Such changes do not alter any legal position of holders, as no contractual or regulatory rights exist. Holders should not interpret technical updates or governance-related changes as amendments to legally binding entitlements.

G.4 Future public offers

This white paper refers to admission to trading. The issuer reserves the right to make further offers in the future. This means that future public offers cannot be ruled out, although there are no current plans to do so.

G.5 Issuer retained crypto-assets

The allocation of GOATED tokens is divided across several categories. Approximately 15.58% is reserved for investors, 7% for airdrop distributions, 15% for the treasury, 20% for the team and early contributors, 3% for advisors and key partners, and 39.42% for the mining pool reserve.

As a result, the effective circulating supply of the token will not correspond to the full allocation immediately, but will change over time depending on how vesting schedules and release mechanisms introduce tokens into the market. These mechanisms can influence token availability and thereby impact market dynamics.

Although there is no formal issuer, certain allocations — in particular the treasury (15%), the team and early contributors (20%), and advisors and key partners (3%) — can, in a broader interpretation, be considered issuer-related. Taken together, these categories represent approximately 38% of the overall supply.

The investor must be aware that a public address cannot necessarily be assigned to a single person or entity, which limits the ability to determine exact economic influence or future actions. Token distribution changes can negatively impact the investor.

G.6 Utility token classification

No

G.7 Key features of goods/services of utility tokens

Not applicable.

G.8 Utility tokens redemption

Not applicable.

G.9 Non-trading request

The admission to trading is sought.

G.10 Crypto-assets purchase or sale modalities

Not applicable, as this white paper is written to support admission to trading and not for the initial offer to the public.

G.11 Crypto-assets transfer restrictions

The crypto-assets as such do not have any transfer restrictions and are generally freely transferable. The Crypto Asset Service Providers can impose their own restrictions in agreements they enter with their clients. The Crypto Asset Service Providers may impose restrictions to buyers and sellers in accordance with applicable laws and internal policies and terms.

G.12 Supply adjustment protocols

No, there are no fixed protocols that can increase or decrease the supply implemented as of 2025-09-07. Also, it is possible to decrease the circulating supply, by transferring crypto-assets to so called "burn-addresses", which are addresses that render the cryptoasset "non-transferable" after sent to those addresses.

G.13 Supply adjustment mechanisms

For the crypto-asset in scope, the supply is limited to 1,000,000,000 tokens. Investors should note that changes in the token supply can have a negative impact.

G.14 Token value protection schemes

No, the token does not have value protection schemes.

G.15 Token value protection schemes description

Not applicable.

G.16 Compensation schemes

No, the token does not have compensation schemes.

G.17 Compensation schemes description

Not applicable.

G.18 Applicable law

Applicable law likely depends on the location of any particular transaction with the token.

G.19 Competent court

Competent court likely depends on the location of any particular transaction with the token.

H.1 Distributed ledger technology (DTL)

See F.13.

H.2 Protocols and technical standards

The crypto-asset is issued and operates on the GOAT Network, a Proof-of-Stake blockchain that is designed as a Layer-2 solution anchored to the Bitcoin mainnet. Consensus is maintained by sequencer nodes that stake both wrapped BTC and the native GOATED token. Transaction fees are paid in wrapped BTC, while the GOATED token is used for staking and block production. The anchoring mechanism to the Bitcoin network is planned as part of the protocol’s further development, but the exact technical implementation and the connection between the two networks are still in progress. The network additionally integrates cross-chain bridges, enabling the transfer and use of assets from external blockchains.

H.3 Technology used

The crypto-asset operates on the GOAT Network, which functions as a distributed ledger maintained by sequencer nodes under a Proof-of-Stake model. The network records token transactions and related activities in a decentralized ledger intended to ensure transparency and security. Users access and manage their assets through cryptographic key pairs, with private key management being essential to safeguard holdings.

The anchoring of state data to the Bitcoin mainnet is part of the planned development but has not yet been fully implemented.

H.4 Consensus mechanism

The network applies a Proof-of-Stake consensus model. Sequencer nodes are required to stake both the native GOATED token and wrapped BTC in order to participate in block production and validation. The weighting of these staked assets determines the ability of nodes to propose and confirm new blocks. The consensus process is designed to align economic incentives with the integrity of the network. The anchoring of consensus states to the Bitcoin mainnet is foreseen but remains under development.

H.5 Incentive mechanisms and applicable fees

Incentives for sequencer nodes primarily derive from transaction fees paid in wrapped BTC and the GOATED tokens as the block production rewards. By securing transactions and producing valid blocks, participating nodes receive these fees as compensation for their role in the system. The GOATED token is not used as a gas token but functions as part of the staking mechanism. Transaction fees within the network are variable and depend on usage levels. As network adoption evolves, the scope and magnitude of incentives may change. No guarantee can be given regarding the level or sustainability of future rewards.

H.6 Use of distributed ledger technology

No, DLT is neither operated by the issuer nor a third party acting on the issuer’s behalf.

H.7 DLT functionality description

Not applicable.

H.8 Audit

As we are understanding the question relating to "technology" to be interpreted in a broad sense, the answer to whether an audit of "the technology used" was conducted is "no, we cannot guarantee, that all parts of the technology used have been audited". This is due to the fact this report focusses on risk, and we cannot guarantee that each part of the technology used was audited.

H.9 Audit outcome

Not applicable.

I.1 Offer-related risks

1. Regulatory and Compliance

This white paper has been prepared with utmost caution; however, uncertainties in the regulatory requirements and future changes in regulatory frameworks could potentially impact the token's legal status and its tradability. There is also a high probability that other laws will come into force, changing the rules for the trading of the token. Therefore, such developments shall be monitored and acted upon accordingly.

2. Operational and Technical

Blockchain Dependency: The token is entirely dependent on the blockchain the cryptoasset is issued upon. Any issues, such as downtime, congestion, or security vulnerabilities within the blockchain, could adversely affect the token's functionality.

Smart Contract Risks: Smart contracts governing the token may contain hidden vulnerabilities or bugs that could disrupt the token offering or distribution processes.

Connection Dependency: As the trading of the token also involves other trading venues, technical risks such as downtime of the connection or faulty code are also possible.

Human errors: Due to the irrevocability of blockchain-transactions, approving wrong transactions or using incorrect networks/addresses will most likely result in funds not being accessibly anymore.

Custodial risk: When admitting the token to trading, the risk of losing clients assets due to hacks or other malicious acts is given. This is due to the fact the token is hold in custodial wallets for the customers.

3. Market and Liquidity

Volatility: The token will most likely be subject to high volatility and market speculation. Price fluctuations could be significant, posing a risk of substantial losses to holders.

Liquidity Risk: Liquidity is contingent upon trading activity levels on decentralized exchanges (DEXs) and potentially on centralized exchanges (CEXs), should they be involved. Low trading volumes may restrict the buying and selling capabilities of the tokens.

4. Counterparty

As the admission to trading involves the connection to other trading venues, counterparty risks arise. These include, but are not limited to, the following risks:

General Trading Platform Risk: The risk of trading platforms not operating to the highest standards is given. Examples like FTX show that especially in nascent industries, compliance and oversight-frameworks might not be fully established and/or enforced.

Listing or Delisting Risks: The listing or delisting of the token is subject to the trading partners internal processes. Delisting of the token at the connected trading partners could harm or completely halt the ability to trade the token.

5. Liquidity

Liquidity of the token can vary, especially when trading activity is limited. This could result in high slippage when trading a token.

6. Failure of one or more Counterparties

Another risk stems from the internal operational processes of the counterparties used. As there is no specific oversight other than the typical due diligence check, it cannot be guaranteed that all counterparties adhere to the best market standards.

Bankruptcy Risk: Counterparties could go bankrupt, possibly resulting in a total loss of the clients’ assets held at that counterparty.

7. Information asymmetry

Different groups of participants may not have the same access to technical details or governance information, leading to uneven decision-making and potential disadvantages for less informed investors.

I.2 Issuer-related risks

1. Insolvency

As with every other commercial endeavor, the risk of insolvency of entities involved in the project is given. This could be caused by but is not limited to lack of interest from the public, lack of funding, incapacitation of key developers and project members, force majeure (including pandemics and wars) or lack of commercial success or prospects.

2. Counterparty

In order to operate, entities involved in the project have most likely engaged in different business relationships with one or more third parties on which they and the network strongly depend on. Loss or changes in the leadership or key partners of entities involved in the project and/or the respective counterparties can lead to disruptions, loss of trust, or project failure. This could result in a total loss of economic value for the crypto-asset holders.

3. Legal and Regulatory Compliance

Cryptocurrencies and blockchain-based technologies are subject to evolving regulatory landscapes worldwide. Regulations vary across jurisdictions and may be subject to significant changes. Non-compliance can result in investigations, enforcement actions, penalties, fines, sanctions, or the prohibition of the trading of the crypto-asset impacting its viability and market acceptance. This could also result in entities involved in the project to be subject to private litigation. The aforementioned would most likely also lead to changes with respect to trading of the crypto-asset that may negatively impact the value, legality, or functionality of the crypto-asset.

4. Operational

Failure to develop or maintain effective internal control, or any difficulties encountered in the implementation of such controls, or their improvement could harm the business, causing disruptions, financial losses, or reputational damage of entities involved in the project.

5. Industry

The network and all entities involved in the project are and will be subject to all of the risks and uncertainties associated with a crypto-project, where the token issued has zero intrinsic value. History has shown that most of these projects resulted in financial losses for the investors and were only set-up to enrich a few insiders with the money from retail investors.

6. Reputational

The network and all entities involved in the project face the risk of negative publicity, whether due to, without limitation, operational failures, security breaches, or association with illicit activities, which can damage the reputation of the network and all entities involved in the project and, by extension, the value and acceptance of the crypto-asset.

7. Competition

There are numerous other crypto-asset projects in the same realm, which could have an effect on the crypto-asset in question.

8. Unanticipated Risk

In addition to the risks included in this section, there might be other risks that cannot be foreseen. Additional risks may also materialize as unanticipated variations or combinations of the risks discussed.

I.3 Crypto-assets-related risks

1. Valuation

As the crypto-asset does not have any intrinsic value, and grants neither rights nor obligations, the only mechanism to determine the price is supply and demand. Historically, most crypto-assets have dramatically lost value and were not a beneficial investment for the investors. Therefore, investing in these crypto-assets poses a high risk, and the loss of funds can occur.

2. Market Volatility

Crypto-asset prices are highly susceptible to dramatic fluctuations influence by various factors, including market sentiment, regulatory changes, technological advancements, and macroeconomic conditions. These fluctuations can result in significant financial losses within short periods, making the market highly unpredictable and challenging for investors. This is especially true for crypto-assets without any intrinsic value, and investors should be prepared to lose the complete amount of money invested in the respective crypto-assets.

3. Liquidity Challenges

Some crypto-assets suffer from limited liquidity, which can present difficulties when executing large trades without significantly impacting market prices. This lack of liquidity can lead to substantial financial losses, particularly during periods of rapid market movements, when selling assets may become challenging or require accepting unfavorable prices.

4. Asset Security

Crypto-assets face unique security threats, including the risk of theft from exchanges or digital wallets, loss of private keys, and potential failures of custodial services. Since crypto transactions are generally irreversible, a security breach or mismanagement can result in the permanent loss of assets, emphasizing the importance of strong security measures and practices.

5. Scams

The irrevocability of transactions executed using blockchain infrastructure, as well as the pseudonymous nature of blockchain ecosystems, attracts scammers. Therefore, investors in crypto-assets must proceed with a high degree of caution when investing in if they invest in crypto-assets. Typical scams include – but are not limited to – the creation of fake crypto-assets with the same name, phishing on social networks or by email, fake giveaways/airdrops, identity theft, among others.

6. Blockchain Dependency

Any issues with the blockchain used, such as network downtime, congestion, or security vulnerabilities, could disrupt the transfer, trading, or functionality of the crypto-asset.

7. Smart Contract Vulnerabilities

The smart contract used to issue the crypto-asset could include bugs, coding errors, or vulnerabilities which could be exploited by malicious actors, potentially leading to asset loss, unauthorized data access, or unintended operational consequences.

8. Privacy Concerns

All transactions on the blockchain are permanently recorded and publicly accessible, which can potentially expose user activities. Although addresses are pseudonymous, the transparent and immutable nature of blockchain allows for advanced forensic analysis and intelligence gathering. This level of transparency can make it possible to link blockchain addresses to real-world identities over time, compromising user privacy.

9. Regulatory Uncertainty

The regulatory environment surrounding crypto-assets is constantly evolving, which can directly impact their usage, valuation, and legal status. Changes in regulatory frameworks may introduce new requirements related to consumer protection, taxation, and antimoney laundering compliance, creating uncertainty and potential challenges for investors and businesses operating in the crypto space. Although the crypto-asset do not create or confer any contractual or other obligations on any party, certain regulators may nevertheless qualify the crypto-asset as a security or other financial instrument under their applicable law, which in turn would have drastic consequences for the crypto-asset, including the potential loss of the invested capital in the asset. Furthermore, this could lead to the sellers and its affiliates, directors, and officers being obliged to pay fines, including federal civil and criminal penalties, or make the crypto-asset illegal or impossible to use, buy, or sell in certain jurisdictions. On top of that, regulators could take action against the network and all entities involved in the project as well as the trading platforms if the regulators view the token as an unregistered offering of securities or the operations otherwise as a violation of existing law. Any of these outcomes would negatively affect the value and/or functionality of the crypto-asset and/or could cause a complete loss of funds of the invested money in the crypto-asset for the investor.

10. Counterparty risk

Engaging in agreements or storing crypto-assets on exchanges introduces counterparty risks, including the failure of the other party to fulfill their obligations. Investors may face potential losses due to factors such as insolvency, regulatory non-compliance, or fraudulent activities by counterparties, highlighting the need for careful due diligence when engaging with third parties.

11. Reputational concerns

Crypto-assets are often subject to reputational risks stemming from associations with illegal activities, high-profile security breaches, and technological failures. Such incidents can undermine trust in the broader ecosystem, negatively affecting investor confidence and market value, thereby hindering widespread adoption and acceptance.

12. Technological Innovation

New technologies or platforms could render the network's design less competitive or even break fundamental parts (i.e., quantum computing might break cryptographic algorithms used to secure the network), impacting adoption and value. Participants should approach the crypto-asset with a clear understanding of its speculative and volatile nature and be prepared to accept these risks and bear potential losses, which could include the complete loss of the asset's value.

13. Community and Narrative

As the crypto-asset has no intrinsic value, all trading activity is based on the intended market value is heavily dependent on its community.

14. Interest Rate Change

Historically, changes in interest, foreign exchange rates, and increases in volatility have increased credit and market risks and may also affect the value of the crypto-asset. Although historic data does not predict the future, potential investors should be aware that general movements in local and other factors may affect the market, and this could also affect market sentiment and, therefore most likely also the price of the crypto-asset.

15. Taxation

The taxation regime that applies to the trading of the crypto-asset by individual holders or legal entities will depend on the holder’s jurisdiction. It is the holder’s sole responsibility to comply with all applicable tax laws, including, but not limited to, the reporting and payment of income tax, wealth tax, or similar taxes arising in connection with the appreciation and depreciation of the crypto-asset.

16. Anti-Money Laundering/Counter-Terrorism Financing

It cannot be ruled out that crypto-asset wallet addresses interacting with the crypto-asset have been, or will be used for money laundering or terrorist financing purposes, or are identified with a person known to have committed such offenses.

17. Market Abuse

It is noteworthy that crypto-assets are potentially prone to increased market abuse risks, as the underlying infrastructure could be used to exploit arbitrage opportunities through schemes such as front-running, spoofing, pump-and-dump, and fraud across different systems, platforms, or geographic locations. This is especially true for crypto-assets with a low market capitalization and few trading venues, and potential investors should be aware that this could lead to a total loss of the funds invested in the crypto-asset.

18. Timeline and Milestones

Critical project milestones could be delayed by technical, operational, or market challenges.

19. Legal ownership: Depending on jurisdiction, token holders may not have enforceable legal rights over their holdings, limiting avenues for recourse in disputes or cases of fraud.

20. Jurisdictional blocking: Access to exchanges, wallets, or interfaces may be restricted based on user location or regulatory measures, even if the token remains transferable on-chain.

21. Token concentration: A large proportion of tokens held by a few actors could allow price manipulation, governance dominance, or sudden sell-offs impacting market stability.

22. Ecosystem incentive misalignment: If validator, developer, or user rewards become unattractive or distorted, network security and participation could decline.

23. Governance deadlock: Poorly structured or fragmented governance processes may prevent timely decisions, creating delays or strategic paralysis.

24. Compliance misalignment: Features or delivery mechanisms may unintentionally conflict with evolving regulations, particularly regarding consumer protection or data privacy.

I.4 Project implementation-related risks

As this white paper relates to the "Admission to trading" of the crypto-asset, the implementation risk is referring to the risks on the Crypto Asset Service Providers side. These can be, but are not limited to, typical project management risks, such as keypersonal-risks, timeline-risks, and technical implementation-risks.

I.5 Technology-related risks

As this white paper relates to the "Admission to trading" of the crypto-asset, the technology-related risks mainly involve the DLT networks where the crypto asset is issued in.

1. Blockchain Dependency Risks

Network Downtime: Potential outages or congestion on the involved blockchains could interrupt on-chain token transfers, trading, and other functions.

2. Smart Contract Risks

Vulnerabilities: The smart contract governing the token could contain bugs or vulnerabilities that may be exploited, affecting token distribution or vesting schedules.

3. Wallet and Storage Risks

Private Key Management: Token holders must securely manage their private keys and recovery phrases to prevent permanent loss of access to their tokens, which includes Trading-Venues, who are a prominent target for dedicated hacks.

Compatibility Issues: The tokens require compatible wallets for storage and transfer. Any incompatibility or technical issues with these wallets could impact token accessibility.

4. Network Security Risks

Attack Risks: The blockchains may face threats such as denial-of-service (DoS) attacks or exploits targeting its consensus mechanism, which could compromise network integrity.

Centralization Concerns: Although claiming to be decentralized, the relatively smaller number of validators/concentration of stakes within the networks compared to other blockchains might pose centralization risks, potentially affecting network resilience.

5. Evolving Technology Risks: Technological Obsolescence: The fast pace of innovation in blockchain technology may make the used token standard appear less competitive or become outdated, potentially impacting the usability or adoption of the token.

6. Bridges: The dependency on multiple ecosystems can negatively impact investors. This asset bridge creates corresponding risks for investors, as this lock-in mechanism may not function properly for technical reasons or may be subject to attack. In that case, the supply may change immediately or the ownership rights to tokens may be changed.

7. Forking risk: Network upgrades may split the blockchain into separate versions, potentially creating duplicate tokens or incompatibility between different versions of the protocol.

8. Economic abstraction: Mechanisms such as gas relayers or wrapped tokens may allow users to bypass the native asset, reducing its direct demand and weakening its economic role.

9. Dust and spam attacks: Low-value transactions may flood the network, increasing ledger size, reducing efficiency, and exposing user addresses to tracking.

10. Frontend dependency: If users rely on centralised web interfaces or wallets, service outages or compromises could block access even if the blockchain itself continues to operate.

I.6 Mitigation measures

None.

J.1 Adverse impacts on climate and other environment-related adverse impacts

S.1 Name

GOAT Foundation

S.2 Relevant legal entity identifier

Not applicable.

S.3 Name of the cryptoasset

GOAT Network Token

S.4 Consensus Mechanism

The network applies a Proof-of-Stake consensus model. Sequencer nodes are required to stake both the native GOATED token and wrapped BTC in order to participate in block production and validation. The weighting of these staked assets determines the ability of nodes to propose and confirm new blocks. The consensus process is designed to align economic incentives with the integrity of the network. The anchoring of consensus states to the Bitcoin mainnet is foreseen but remains under development.

S.5 Incentive Mechanisms and Applicable Fees

Incentives for sequencer nodes primarily derive from transaction fees paid in wrapped BTC and the GOATED tokens as the block production rewards. By securing transactions and producing valid blocks, participating nodes receive these fees as compensation for their role in the system. The GOATED token is not used as a gas token but functions as part of the staking mechanism. Transaction fees within the network are variable and depend on usage levels. As network adoption evolves, the scope and magnitude of incentives may change. No guarantee can be given regarding the level or sustainability of future rewards.

S.6 Beginning of the period to which the disclosure relates

2024-09-10

S.7 End of the period to which the disclosure relates

2025-09-10

S.8 Energy consumption

19710.52532 kWh/a

S.9 Energy consumption sources and methodologies

The energy consumption of this asset is aggregated across multiple components: To determine the energy consumption of a token, the energy consumption of the network GOAT is calculated first. For the energy consumption of the token, a fraction of the energy consumption of the network is attributed to the token, which is determined based on the activity of the crypto-asset within the network. When calculating the energy consumption, the Functionally Fungible Group Digital Token Identifier (FFG DTI) is used - if available - to determine all implementations of the asset in scope. The mappings are updated regularly, based on data of the Digital Token Identifier Foundation. The information regarding the hardware used and the number of participants in the network is based on assumptions that are verified with best effort using empirical data. In general, participants are assumed to be largely economically rational. As a precautionary principle, we make assumptions on the conservative side when in doubt, i.e. making higher estimates for the adverse impacts.

S.10 Renewable energy consumption

32.9773820633 %

S.11 Energy intensity

0.00006 kWh

S.12 Scope 1 DLT GHG emissions – Controlled

0.00000 tCO2e/a

S.13 Scope 2 DLT GHG emissions – Purchased

6.55992 tCO2e/a

S.14 GHG intensity

0.00002 kgCO2e

S.15 Key energy sources and methodologies

To determine the proportion of renewable energy usage, the locations of the nodes are to be determined using public information sites, open-source crawlers and crawlers developed in-house. If no information is available on the geographic distribution of the nodes, reference networks are used which are comparable in terms of their incentivization structure and consensus mechanism. This geo-information is merged with public information from Our World in Data, see citation. The intensity is calculated as the marginal energy cost wrt. one more transaction. Ember (2025); Energy Institute - Statistical Review of World Energy (2024) - with major processing by Our World in Data. “Share of electricity generated by renewables - Ember and Energy Institute” [dataset]. Ember, “Yearly Electricity Data Europe”; Ember, “Yearly Electricity Data”; Energy Institute, “Statistical Review of World Energy” [original data]. Retrieved from https://ourworldindata.org/grapher/share-electricity-renewables.

S.16 Key GHG sources and methodologies

To determine the GHG Emissions, the locations of the nodes are to be determined using public information sites, open-source crawlers and crawlers developed in-house. If no information is available on the geographic distribution of the nodes, reference networks are used which are comparable in terms of their incentivization structure and consensus mechanism. This geo-information is merged with public information from Our World in Data, see citation. The intensity is calculated as the marginal emission wrt. one more transaction. Ember (2025); Energy Institute - Statistical Review of World Energy (2024) - with major processing by Our World in Data. “Carbon intensity of electricity generation - Ember and Energy Institute” [dataset]. Ember, “Yearly Electricity Data Europe”; Ember, “Yearly Electricity Data”; Energy Institute, “Statistical Review of World Energy” [original data]. Retrieved from https://ourworldindata.org/grapher/carbon-intensity-electricity Licensed under CC BY 4.0.